Every year, JPMorgan (JPM) comes out with its annual guide to retirement with insights about trends and outlook to benefit the people that use the company’s asset management platform as retirees or advisers.

The guide published recently, but it pre-dates the coronavirus crisis that has slammed the economy and sent the markets spiraling, stressing those saving or in retirement.

Katherine Roy, JPMorgan’s chief retirement strategist and the person behind much of the guide, shared thoughts on what she’s learned from coronavirus crisis so far — and things to keep in mind.

‘Focus on what you can control’

Roy said this is a key message JPMorgan is sharing with companies that sponsor 401(k) plans for their employees.

“Saving is one of those pieces,” Roy says. “In a time where there’s such volatility in the market and uncertainty in Washington, focus on what you can control.”

One idea she has for this is saving transportation expenses if you’re stuck at home as well as money that might ordinarily go to eating out.

“Take a fresh look at your spending,” she said. “Most people commute quite a bit. Looking for an opportunity to redirect that money thoughtfully is important.”

A lot of ink has been spilled bemoaning the fact that many Americans don’t have adequate emergency savings; Roy says this could be an opportunity to shore some of that up. Furthermore, it’s not just for people who are struggling to make ends meet, but also for people who invest all their money. Putting all your savings in illiquid investments is risky – if an unexpected expense comes up, you might have to sell when the market’s down to get cash fast. For those people, Roy says, this should be a wakeup call.

The 401(k) system works pretty well

Data from Roy’s team showed that during 2008 and 2009, 97% of workers continued to make 401(k) contributions and 85% didn’t change their allocations or investment directions.

To retirement strategists, this is a good thing.

“The 401(k) system, in terms of inertia, we saw it really hold up well,” Roy says. “The 401(k) balances surpassed their 2007 levels by the end of 2010. The feeling is that it took a lot longer to recover.”

There’s other aspects in the design that are paying off as well, like having automatic opt-in, automatic annual increases, and having the default being a target date fund that automates investment allocation. Since people really don’t touch their 401(k) often, all of this pushes people towards recommended behavior.

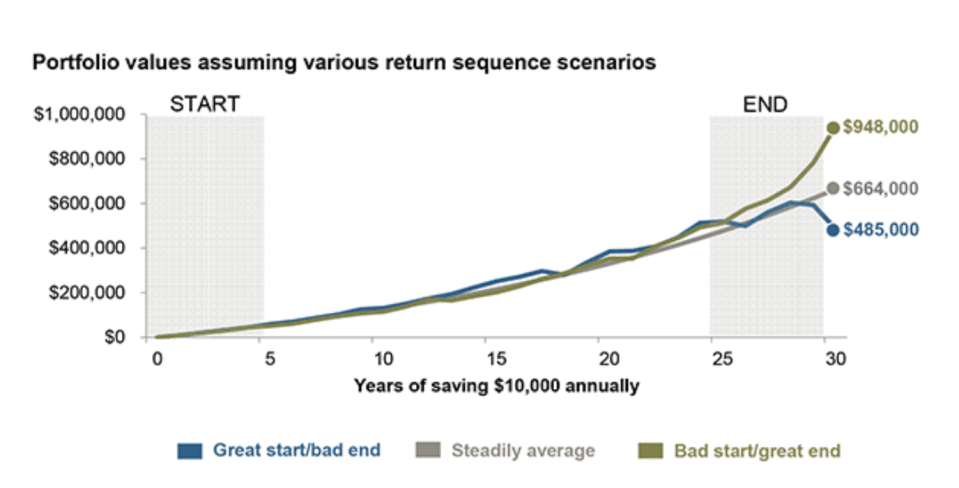

De-risk when it’s time to de-risk

According to Fidelity data, 57% of baby boomers who manage their own money should be changing their asset allocations to match their risk tolerance.

One great thing about target date funds — the default fund option in most 401(k) plans — is that they automatically lower the exposure to riskier assets as a person ages. This is another feature of the system, Roy says, but if you manage your own money, it’s on you.

“You want to make sure you make the de-risking decisions in advance when wealth is greatest,” says Roy. The key here is to learn to de-risk proactively.

The reason is explained in the annual guide to retirement via a handy chart with a caption that says “the greatest risk is when wealth is the greatest.”

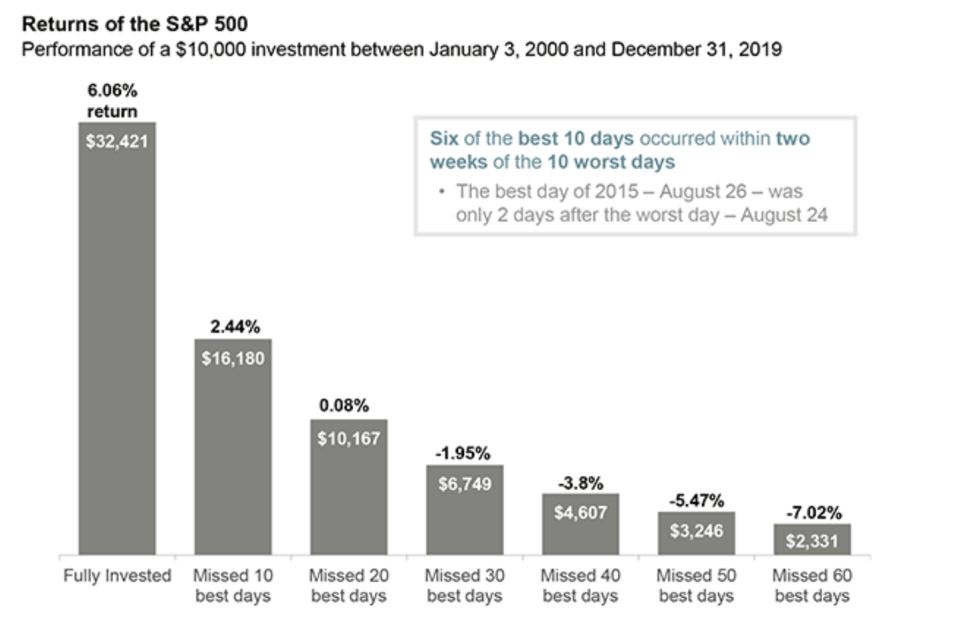

The market isn’t just down — it’s extremely volatile

Roy and many other retirement professionals point to the past to show that things usually recover within a few years.

“The bad news: Few investors are good at trading around extreme market volatility,” Tony DeSpirito, CIO of US Fundamental Activity Equity at BlackRock and Portfolio Manager of the BlackRock Equity Dividend Fund, wrote in a recent blog post. “The good news: decades of stock market history tell us “this too shall pass.”

But beyond that, Roy stresses that people should understand how volatile things are and what that means — you can’t know whether today is going to be a good day or not.

“One of the most popular charts [in the retirement guide] is the impact of being out of the market,” she said. “The idea you’re going to know when to get in is virtually impossible.”

You don’t want to miss the best days, and they might be next to some of the worst as well, she said.

“Stay contributing and you might be buying some of the lowest days, but you’ll be buying some of the highest, too,” she said.

---

Ethan Wolff-Mann is a writer at Yahoo Finance focusing on consumer issues, personal finance, retail, airlines, and more. Follow him on Twitter @ewolffmann.

Coronavirus ‘good scenario’ could see 30% of small businesses failCoronavirus could accelerate US cannabis legalization

Here’s how long it usually takes to recover from a bear market

Companies face fresh security risks due to people working from home

Read the latest financial and business news from Yahoo Finance

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, YouTube, and reddit.