5 game-changing papers from this year's largest gathering of economists

Thousands of economists from all over the world convened in Atlanta this weekend to share their research on topics ranging from sovereign debt to water conservation.

Yahoo Finance was on-site for the conference and highlights five big papers that could be game-changers for finance and the field of economics itself.

Time to consider price-level targeting

Paper: “Monetary Policy Frameworks and the Effective Lower Bound”

Author(s): John C. Williams (New York Fed) and Thomas Mertens (San Francisco Fed)

Summary: New York Fed President John Williams headlines a new paper suggesting that policymakers should aim high when targeting their inflation targets to “offset” the tendency for expected inflation to be closer to the lower bound, especially during periods of low interest rates. But Williams goes further, adding that price-level targeting (by setting goals on a price index instead of an inflation figure) would give policymakers more flexibility by allowing inflation to deviate more as long as it keeps prices near-target. Williams has one caveat to price-level targeting: The public needs to believe the Fed and clearly understand its policy for it to work.

Why it’s important: The Federal Open Market Committee currently has a 2% inflation target in pursuit of its mandate of price stability. But the Fed has had issues stimulating inflation, which Williams partly attributes to a “downward bias” in market participants treating the 2% inflation target as a ceiling — despite Fed communications making it clear that the target is “symmetric.” Price-level targeting would allow inflation to more freely deviate as long as the prices themselves remain stable, without the issue of “symmetric” or “ceiling-level” targets. His suggestion comes as the Fed gets ready to revise its communications and strategies, meaning that Williams could make the case for actually effecting this change soon.

Key quote: “[W]e find that price-level targeting dominates average-inflation target because the former creates expectations of relatively high inflation and output gaps following periods when the lower bound is binding.”

Don’t panic over the inverting yield curve

Author(s): Azhar Iqbal (Wells Fargo Securities), Sam Bullard (Wells Fargo Securities), Shannon Seery (Wells Fargo Securities)

Summary: Market observers looking for a sign of a recession often point to an inverting yield curve. Since 1969, all recessions have been preceded by the yield on the 10-year Treasury falling below below the yield on the 2-year Treasury. But Iqbal, Bullard, and Seery propose a new model that’s able to predict all recessions as far back as 1954: looking at the spread between the federal funds rate and the 10-year bond. Their model suggests a high probability of a recession in 2019.

Why it’s important: The tightening spread between the 10-year and the 2-year has markets worried about a yield curve inversion very soon. In early December, the 5-year dipped below the 2-year. But the paper argues that low interest rates make it hard for already-low yield longer-term Treasurys to fall below shorter-term Treasurys. The takeaway: The yield curve may never invert in this cycle, but the economy is still at risk of a recession with the 10-year yield (2.659% as of Friday) approaching the target federal funds rate (between 2.25% and 2.50%).

Key quote: “With our framework, we do not have to wait for the yield curve to invert (or peaking of the fed funds rate) to predict a recession.”

Watch out for China

Paper: “China vs. US: IMS Meets IPS”

Author(s): Emmanuel Farhi (Harvard) and Matteo Maggiori (Harvard)

Summary: Farhi and Maggiori write that China’s growing trade relationships with other countries threatens the dominance of the U.S. dollar. Their paper, which will be published this week, argues that as more goods get priced in renminbi, the more the U.S. dollar faces depreciating pressure, which in turn could force the U.S. to reduce debt. Farhi and Maggiori write that if this chain of events occurs, the U.S. dollar could lose its perception as a safe asset and cause the entire international monetary system to destabilize.

Why it’s important: Although the U.S.-China trade talks have generated a lot of headline risk, Farhi’s and Maggiori’s paper casts light on how the U.S. could still end up the loser in China’s relationships with other countries. Consider Brazil, for example, a strong business partner of China’s. Most global firms invoice the sale of goods in U.S. dollars, simply because it is the most trusted and held currency in the world. But as China continues to build its network of strategic partnerships around the world, business partners like Brazil are ramping up the amount of goods they choose to invoice in renminbi. Farhi and Maggiori argue that if the U.S. dollar loses its share of use in invoicing, it could destabilize the currency and threaten the perception of U.S. debt as a safe asset.

Key quote: “You see a worrisome combination.” — Maggiori on the U.S. shrinking in its international engagement as U.S. debt continues to increase.

Balancing the gender scale in economics

Paper: How Can Economics Solve Its Gender Problem?

Author(s): Janet Yellen (former Fed Chair), Susan Athey (Stanford), Sebnem Kalemli-?zcan (University of Maryland), Marianne Bertrand (University of Chicago)

Summary: Although they did not technically work together on a paper, Yellen joined Athey, Kalemli-?zcan, and Bertrand for a panel discussion asking why the economics field has been so difficult to navigate for women. All panelists said that economics has been more accessible to women than it used to be, but noted that progress has stagnated as-of late. They said that women have noted harsher treatment than their male counterparts in seminars, had difficulty taking maternity leave, and generally feel less free to openly share ideas because of the male dominance in the university and professional settings.

Why it’s important: Data from the American Economic Association confirms that little progress has been made in female representation in the economics field. In 1993, only 30.4% of all first-year Ph.D students were women. In 2017, that figure had only ticked up to 32.3%. Throughout the history of the Nobel Prize for economics, only one woman has ever won. But the last few months have been particularly difficult for women in the AEA specifically. The organization announced it would add Harvard professor Roland Fryer to its executive committee and then faced enormous backlash as details surfaced that both Massachusetts and Harvard were investigating allegations of sexual harassment against him. Fryer ultimately “resigned” from the committee, but some AEA members expressed disappointment with the organization over its handling of the situation.

Key quote: “In academia, and in research in general, you have huge power imbalances where young people are much dependent on senior person who can ruin their lives or make their career. And I find it completely natural that women would be very hesitant to want to be viewed as troublemakers and to disrupt those relationships” — Janet Yellen

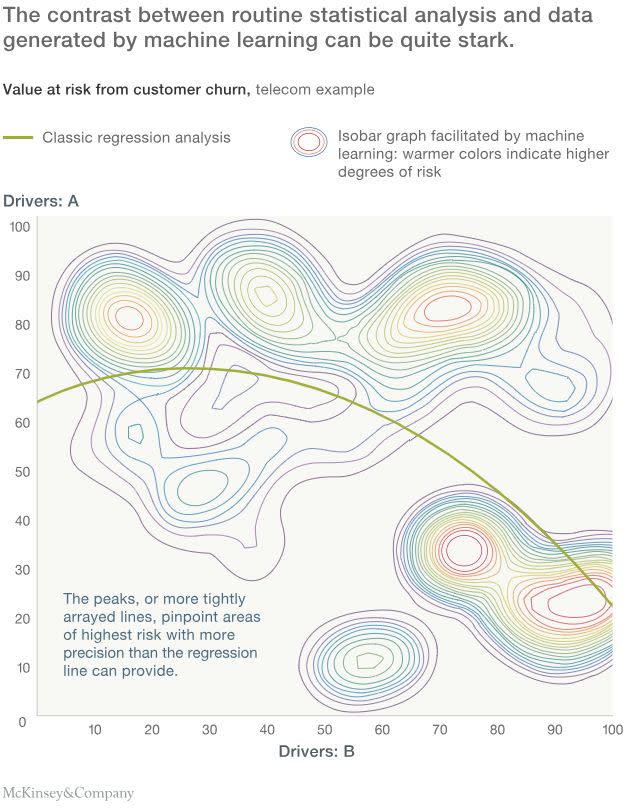

Smarter algorithms for smarter policy

Paper: “The Impact of Machine Learning on Econometrics and Economics”

Author(s): Susan Athey (Stanford)

Summary: Economics has relied on the “classical regression analysis” for the longest time, which models the relationship of a certain amount of variables to make forecasts about theoretical observations. But Athey has blown up the entire economics field by suggesting that a far better econometric model exists out there: dynamic “machine learning.” Athey argues that by feeding rounds of data into smarter algorithms, economists could create models powerful enough to make predictions in never-experienced scenarios and even produce unobserved or unexpected outcomes.

Why it’s important: Machine learning could do a far better job at explaining and forecasting complex human behavior than existing models like linear regression, which would have far-reaching implications for businesses and policymakers. One example: Athey used scanner data from supermarkets to draw conclusions about the optimal pricing of a product and whether or not giving a 30% coupon to a targeted selection of shoppers would improve profits. Athey has said machine learning would be a better guide for a wide-range of decision-making, from helping patients seek healthcare to guiding customers to the right financial products for their personal goals.

Key quote: “[T]he combination of ML and newly available datasets will change economics in fairly fundamental ways, ranging from new questions, to new approaches to collaboration (larger teams and interdisciplinary interaction), to a change in how involved economists are in the engineering and implementation of policies.”

Brian Cheung is a reporter covering the banking industry and the intersection of finance and policy for Yahoo Finance. You can follow him on Twitter @bcheungz.

Read more:

Wells Fargo economist: It's time to abandon the yield curve

Fed Chair Powell communicates that monetary policy is not on autopilot

Warren turns up rhetoric against Wall Street in 2020 bid

Leveraged loans aren't as attractive as they used to be

Congress may have accidentally freed nearly all banks from the Volcker Rule