adidas And 2 More German Stocks That Could Be Trading Below Their Estimated Value

As European inflation nears the central bank's target, Germany’s DAX has reached new highs, reflecting optimism in the market. Despite some caution from policymakers and mixed economic sentiment, there are opportunities for investors to find undervalued stocks that could offer significant value. In this context, identifying a good stock often involves looking at companies with strong fundamentals and growth potential that may not yet be fully appreciated by the market. This article will explore adidas and two other German stocks that could be trading below their estimated value.

Top 10 Undervalued Stocks Based On Cash Flows In Germany

Name | Current Price | Fair Value (Est) | Discount (Est) |

MBB (XTRA:MBB) | €99.50 | €195.06 | 49% |

technotrans (XTRA:TTR1) | €17.15 | €31.42 | 45.4% |

Gerresheimer (XTRA:GXI) | €104.50 | €192.46 | 45.7% |

ecotel communication ag (XTRA:E4C) | €12.80 | €21.95 | 41.7% |

Verbio (XTRA:VBK) | €16.42 | €30.14 | 45.5% |

Schweizer Electronic (XTRA:SCE) | €4.28 | €7.54 | 43.2% |

MTU Aero Engines (XTRA:MTX) | €265.10 | €496.81 | 46.6% |

Dr. H?nle (XTRA:HNL) | €15.45 | €28.57 | 45.9% |

elumeo (XTRA:ELB) | €2.22 | €3.92 | 43.3% |

LPKF Laser & Electronics (XTRA:LPK) | €8.22 | €12.49 | 34.2% |

Let's review some notable picks from our screened stocks.

adidas

Overview: adidas AG, with a market cap of €41.07 billion, designs, develops, produces, and markets athletic and sports lifestyle products across Europe, the Middle East, Africa, North America, Greater China, the Asia-Pacific region, and Latin America.

Operations: The company's revenue segments include €3.26 billion from Greater China, €2.39 billion from Latin America, and €5.07 billion from North America.

Estimated Discount To Fair Value: 17.3%

adidas AG appears undervalued based on cash flows, trading at €230, below its estimated fair value of €278.20. Recent earnings reports show robust growth with Q2 2024 net income at €190 million compared to €84 million a year ago. Revenue is expected to grow at 8.3% annually, outpacing the German market's 5.5%. Earnings are forecasted to grow significantly by 41.8% per year over the next three years, reflecting strong future profitability and return on equity projections of 31.6%.

According our earnings growth report, there's an indication that adidas might be ready to expand.

Take a closer look at adidas' balance sheet health here in our report.

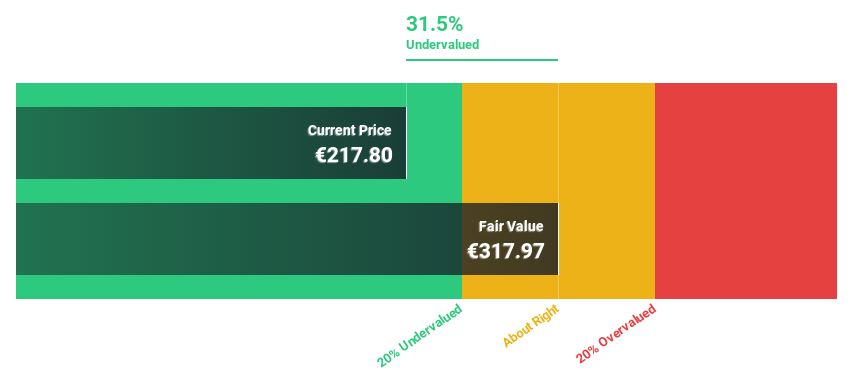

Gerresheimer

Overview: Gerresheimer AG, with a market cap of €3.60 billion, manufactures and sells medicine packaging, drug delivery devices, and solutions in Germany and internationally through its subsidiaries.

Operations: Gerresheimer generates revenue primarily from its Plastics & Devices segment (€1.11 billion) and Primary Packaging Glass segment (€892.01 million), with additional contributions from Advanced Technologies (€6.21 million).

Estimated Discount To Fair Value: 45.7%

Gerresheimer is trading at €104.5, significantly below its estimated fair value of €192.46, indicating it may be undervalued based on cash flows. Despite a high level of debt and a forecasted low return on equity in three years (14.2%), the company’s earnings are expected to grow substantially at 22.3% per year, outpacing the German market's 19.7%. Recent earnings reports show stable performance with Q2 net income slightly down to €32.46 million from €34.43 million last year.

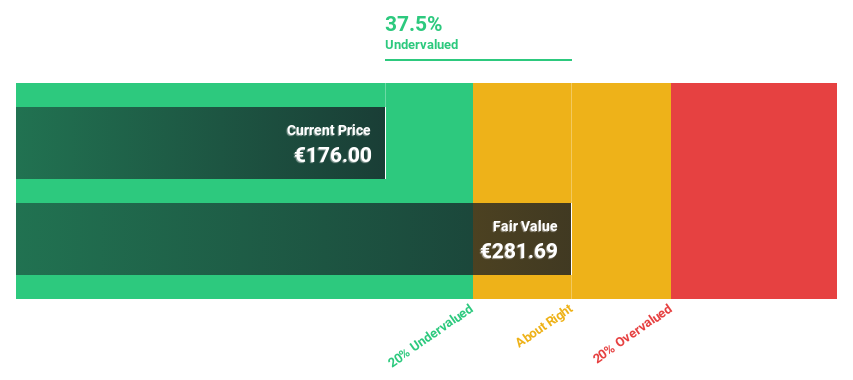

SAP

Overview: SAP SE, along with its subsidiaries, offers applications, technology, and services globally and has a market cap of approximately €231.15 billion.

Operations: SAP SE generates revenue of €32.54 billion from its Applications, Technology & Services segment.

Estimated Discount To Fair Value: 31.1%

SAP SE is trading at €198.2, well below its estimated fair value of €287.65, indicating it is undervalued based on cash flows. Despite recent executive changes and mixed financial results, SAP's earnings are forecast to grow significantly over the next three years at 37.88% annually, outpacing the German market's 19.7%. Recent client wins like Xerox and Kyndryl emphasize SAP’s strong cloud solutions portfolio and potential for future revenue growth, which is expected to be faster than the German market average.

The growth report we've compiled suggests that SAP's future prospects could be on the up.

Dive into the specifics of SAP here with our thorough financial health report.

Taking Advantage

Investigate our full lineup of 21 Undervalued German Stocks Based On Cash Flows right here.

Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready To Venture Into Other Investment Styles?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include XTRA:ADS XTRA:GXI and XTRA:SAP.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]