Arcadis And Two More Stocks On Euronext Amsterdam That May Be Priced Below Estimated Value

As global markets experience fluctuations and various regions show mixed economic signals, the Netherlands' stock market presents unique opportunities for investors looking for value. Amidst broader European economic uncertainties and varying monetary policies, identifying stocks that may be undervalued could offer potential benefits in the current market environment. In this context, understanding key characteristics such as solid fundamentals, strategic positioning within their sectors, and resilience to economic shifts becomes crucial in pinpointing these opportunities.

Top 5 Undervalued Stocks Based On Cash Flows In The Netherlands

Name | Current Price | Fair Value (Est) | Discount (Est) |

Majorel Group Luxembourg (ENXTAM:MAJ) | €29.45 | €55.97 | 47.4% |

PostNL (ENXTAM:PNL) | €1.277 | €2.54 | 49.8% |

Arcadis (ENXTAM:ARCAD) | €59.15 | €114.76 | 48.5% |

Ordina (ENXTAM:ORDI) | €5.70 | €10.64 | 46.4% |

InPost (ENXTAM:INPST) | €16.72 | €30.84 | 45.8% |

Ebusco Holding (ENXTAM:EBUS) | €1.656 | €2.91 | 43% |

Ctac (ENXTAM:CTAC) | €3.18 | €3.83 | 16.9% |

Here we highlight a subset of our preferred stocks from the screener

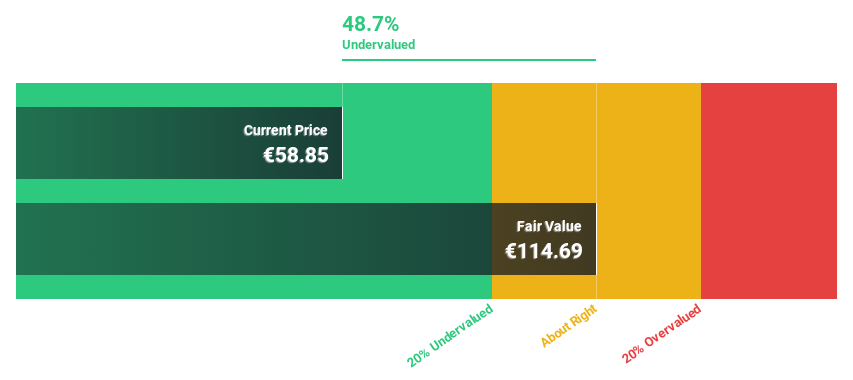

Arcadis

Overview: Arcadis NV is a global company providing design, engineering, and consultancy services for natural and built assets, with a market capitalization of approximately €5.32 billion.

Operations: The company generates revenue through four primary segments: Places (€1.94 billion), Mobility (€978.80 million), Resilience (€1.96 billion), and Intelligence (€122.50 million).

Estimated Discount To Fair Value: 48.5%

Arcadis, priced at €59.15, appears undervalued based on discounted cash flow analysis, with an estimated fair value of €114.76, indicating a potential underpricing of 48.5%. Despite this, its revenue growth is modest at 1.6% annually—slower than the broader Dutch market's 9.7%. However, earnings are expected to increase significantly by 20.72% yearly over the next three years. Recent contracts like leading Enterprise Decision Analytics for Henderson highlight its strategic expansions but it maintains a high level of debt.

The analysis detailed in our Arcadis growth report hints at robust future financial performance.

Take a closer look at Arcadis' balance sheet health here in our report.

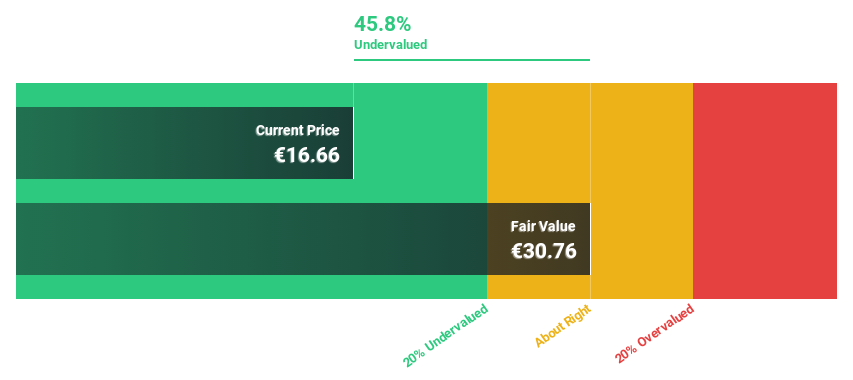

InPost

Overview: InPost S.A., along with its subsidiaries, operates as an out-of-home e-commerce enablement platform offering parcel locker services across Europe, with a market capitalization of approximately €8.36 billion.

Operations: The company generates revenue from two primary segments: Segment Adjustment at PLN 6.35 billion and International - Mondial Relay at PLN 2.92 billion.

Estimated Discount To Fair Value: 45.8%

InPost, trading at €16.72, is valued well below its estimated fair value of €30.84, suggesting a significant undervaluation. The company's earnings have surged by 56.6% over the past year with expectations to grow by 27.9% annually, outpacing the Dutch market forecast of 18%. Despite these strong growth prospects and a very high forecasted Return on Equity of 47.3%, it operates under a high level of debt which could pose risks. Recent presentations and robust quarterly performance underscore its active market engagement and solid financial growth.

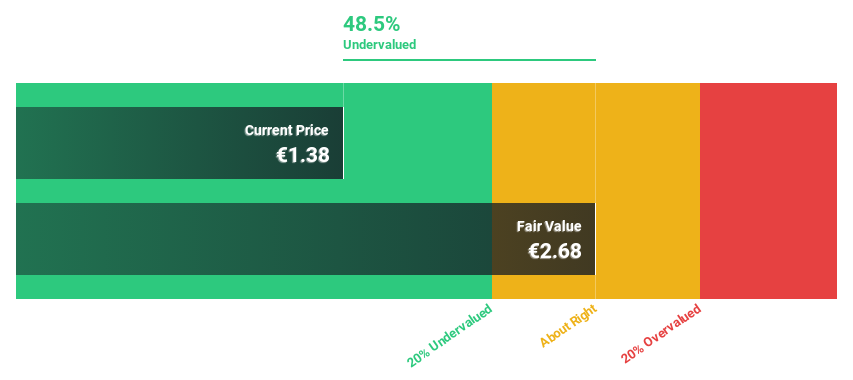

PostNL

Overview: PostNL N.V. offers postal and logistics services across the Netherlands, Europe, and globally, with a market capitalization of approximately €0.64 billion.

Operations: The company generates revenue primarily through two segments: Packages (€2.25 billion) and Mail in the Netherlands (€1.35 billion).

Estimated Discount To Fair Value: 49.8%

PostNL, priced at €1.28, is significantly undervalued against a fair value of €2.54, with its stock trading 49.8% below this estimate. Despite a challenging revenue growth forecast of 3.4% annually—slower than the Dutch market average—the company's earnings are expected to increase by 24.23% per year over the next three years, outperforming the broader market projection of 18%. However, concerns include an unstable dividend history and high debt levels which could impact financial stability.

Taking Advantage

Discover the full array of 7 Undervalued Euronext Amsterdam Stocks Based On Cash Flows right here.

Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Want To Explore Some Alternatives?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ENXTAM:ARCADENXTAM:INPST and ENXTAM:PNL

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]