It’s been a shaky start to the fourth quarter for markets.

After a third quarter that saw stocks enjoy their best run since 2013, each of the major averages finished this week with losses as tech stocks took the biggest hit while a rise in Treasury yields had most of the market’s attention.

On Friday, all three major indices closed red with the Nasdaq pacing losses, falling 1.1% during a week in which the tech index dropped 3.2%. The small-cap Russell 2000 — which dropped 2.5% this week — was down about 0.9% on Friday while the Dow and S&P 500 closed off their lows, though both logged losses greater than 0.5%.

The stock market’s volatility this week was largely dictated by moves from the bond market where yields on U.S. Treasury bonds across the curve moved higher with the 10-year yield finishing the week at 3.23%, the highest level since 2011. Yields moved higher on Friday after the September jobs report showed the U.S. economy remains strong as the unemployment rate moved to a 49-year low of 3.7%, indicating the Fed will likely raise rates once more this year and up to four times in 2019.

“The recent strength of the economy appears to be pushing Fed officials in an increasingly hawkish direction,” said Andrew Hunter, U.S. economist at Capital Economics. “But the corresponding surge in market interest rates this week only reinforces our own view that economic growth will slow sharply next year.”

President Donald Trump on Friday took to Twitter and focused on the current economic expansion — not the potential slowdown in growth Hunter and other economists have discussed — saying simply, “Just out: 3.7% Unemployment is the lowest number since 1969!” Let the good times roll.

In the week ahead, investors will have a bit of an abbreviated schedule with bond markets closed on Monday for Columbus Day — likely keeping volumes down across the Street — while equity markets in the U.S. will be open all five trading days.

China’s Shanghai stock exchange will also re-open on Monday after having been closed this past week for a national holiday. This re-opening comes after shares of a number of Chinese companies listed in the U.S. fell sharply this past week.

On the economic calendar, investors will face a lighter calendar after this past week’s big jobs report with inflation data out Thursday the main highlight. Economists expect that “core” consumer prices, which exclude the cost of food and gas, will rise 2.3% over last year in September. The Fed is targeting 2% inflation.

And on the earnings side, things will start to pick up towards the end of the week with major U.S. banks marking the unofficial start of earnings season as JP Morgan (JPM), Wells Fargo (WFC), Citigroup (C), and PNC Financial (PNC) will all report earnings on Friday.

Elsewhere on the earnings calendar Delta (DAL) and Walgreen’s (WBA) will report results on Thursday.

Economic calendar

Monday: No major economic data set for release.

Tuesday: NFIB small business optimism, September (109 expected; 108.8 previously)

Wednesday: Producer prices, September (+0.2% expected; -0.1% previously)

Thursday: Consumer price index, month-on-month, September (+0.2% expected; +0.2% previously); “Core” consumer price index, year-on-year, September (+2.3% expected; +2.2% previously); Initial jobless claims (207,000 previously)

Friday: Import price index, September (+0.3% expected; -0.6% previously); University of Michigan consumer sentiment, October preliminary reading (100.8 expected; 100.1 previously)

Earnings season will be great, but painful

Earnings season is upon us.

This coming Friday, big U.S. banks including JP Morgan, Citi, and Wells Fargo will report results, kicking off a six-week sprint when most major companies will report quarterly results and markets will get a fresh look at where corporate America stands through three quarters of the year.

And according to data from Bespoke Investment Group, this season is likely to be tough for investors.

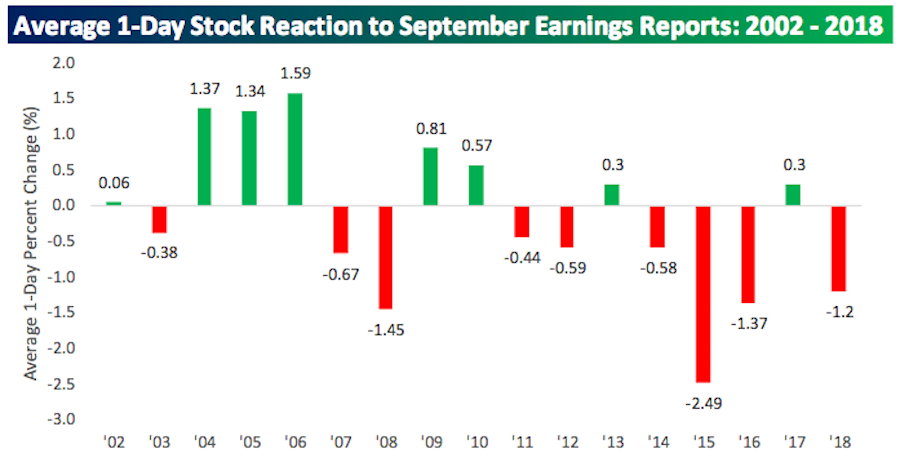

“While this past September was positive for the S&P 500, companies reporting earnings face pretty brutal initial reactions,” Bespoke said in a note to clients on Friday. The firm notes that in September 109 public companies reported results with the average one-day reaction to earnings coming in at a decline of 1.2%. In the second half of the month, the average reaction to the 43 companies that reported earnings was a drop of 3.5%.

Investors are clearly punishing companies who do not meet lofty expectations while the rewards for strong results remain stingy. And though this is a trend that tends to hold during most earnings periods, the market’s current run has had many investors cautious about what the future holds for markets.

What’s notable is that in the third quarter, S&P 500 companies are expected to report great earnings with earnings per share forecast to rise 19.2% during the quarter, according to data from FactSet. And the firm notes that reported earnings are likely to exceed this forecast due to companies reporting positive earnings surprises, thus putting annual earnings growth above 20% for the third straight quarter.

And while these high expectations have created anxiety among investors quick to punish poor results, what September’s trend means for markets over the next few months isn’t entirely clear.

Bespoke finds that after years when the average reaction from investors to a company’s earnings is a drop of 1% or more in the stock, October and November tend to see the same pattern. The anxiety expressed in punishing poor results is not resolved overnight. This clearly indicates an earnings season wherein poor results will be punished harshly.

The broader market implications are somewhat less clear, however, particularly since stocks were up in September.

Since 2002, there have been four years — including 2018 — when the average stock’s reaction to earnings was a decline of 1% or more in September. In the three previous instances the S&P 500 was also lower for the month. This year, however, the benchmark index gained 0.4% in September, pointing to a more broadly favorable environment for stocks though individual companies are not getting a break from investors.

What’s more, in two of the previous three years that stocks dropped more than 1% after earnings in September the S&P 500 actually gained ground in October and November, advancing more than 8% in 2015 and 1.4% in 2016.

Working with just three data points, however, makes teasing out what markets are likely to do over the next few months little more than a guess. But the current mindset in which most investors are operating ought to be somewhat clear.

Expectations for corporations enjoying the benefit of tax cuts are high. Bad quarters are being judged harshly. But the overall market remains in a clear uptrend. Mixed signals for sure, but as Charlie Munger once told Howard Marks, “None of this is meant to be easy, and anybody who thinks it’s easy is stupid.”

—

Myles Udland is a writer at Yahoo Finance. Follow him on Twitter @MylesUdland