Exclusive: Wells Fargo pushed wealth advisors to use high-fee products, cross-sell

For almost two years, Wells Fargo (WFC) has been under near-constant fire. It all began, of course, with the revelation that employees in bank branches, who faced immense pressure to sell, had opened fake accounts for customers. Then, the bank agreed to pay a $1 billion fine to settle allegations of abuses in its auto lending and mortgage businesses.

In the spring, the bank also disclosed that its board was conducting a review of “certain activities” within the bank’s wealth management unit, which filings describe as including fee calculations of fiduciary accounts.

In mid-July, Yahoo Finance reported on increasing sales pressure in the wealth management sector of Wells’s Private Bank. Late last month, the Wall Street Journal also reported that four Wells Fargo advisors had sent a letter to the Justice Department and the Securities and Exchange Commission, detailing “long-standing problems” in the wealth management business.

Now, former advisors in the wealth management area of the Private Bank, which caters to high-net-worth investors, are shedding light on what some of those problems may be. They expressed additional concerns to Yahoo Finance, including Wells encouraging fiduciary advisors to put client money in higher-fee options, requiring advisors to, in effect, cross-sell products like mortgages and financial planning, and push what several former advisors viewed as unnecessary financial planning fees on clients. Internal documents shared with Yahoo Finance corroborate their concerns.

In addition, the Journal reported that the broad class of Wells Fargo advisors were encouraged to funnel wealthier clients into the Private Bank’s wealth management area because the fees were higher. A former senior executive in this area and multiple former Wells Fargo brokers expressed that to Yahoo Finance as well.

In general, Wells Fargo’s interest in boosting its advisory revenue is in step with much of the industry. In the low-interest environment of the past decade, most banks have looked for other ways to bring in revenue, and wealth management products were an obvious choice for expansion. But at Wells Fargo, a number of troubling reports have emerged that cast a less-than-flattering light on this expansion.

“At Wells Fargo Wealth and Investment Management, we are committed to taking care of our clients’ financial needs every day and take seriously our responsibility to help them preserve and invest their hard-earned savings,” says spokesperson Shea Leordeanu. “Our primary goal is to be a trusted advisor to our clients and to act in their best interest.”

Advisors felt pushed to add high-fee products to portfolios

Wells Fargo encouraged its advisors to put their clients’ money in a variety of more complex products, from so-called alternative investments — such as hedge funds or private equity funds — to separately managed accounts, which are portfolios of individual securities. Advisors were also encouraged to use financial tools like options. Some of these came with additional fees.

Such products can be in clients’ best interests. But because advisors say they were encouraged to reach certain quotas for all these products or face hits to their compensation, it raises a question as to whether these fiduciary advisors were serving their clients’ interests — or their own. Fiduciaries must put the interests of the client first.

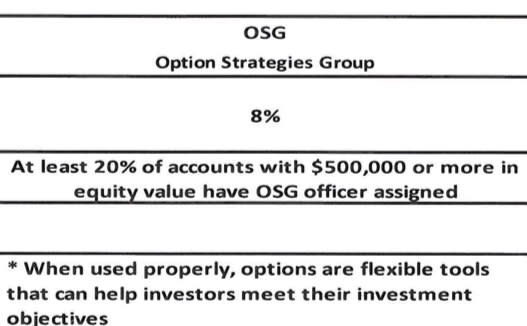

In a presentation document called “IFS Summit: Be The Solution,” from August 2016, Private Bank advisors were told to have “At least 4 private placement purchases per Investment Strategist,” “at least 3 new third party SMA [separately managed accounts] per Investment Strategist,” and “At least 20% of accounts with $500,000 or more in equity value have OSG [options strategies group] officer assigned.”

The “strategy” that troubled one former advisor most was for options, which carried some of the highest fees. Advisors were obligated to have an “options strategy officer” for 20% of accounts that had over $500,000 worth of equities, according to the documents and former advisors.

According to fee schedules, fees for options — managed collars, long calls, call and put spreads, and non-single-stock call writing — carried additional fees of 0.50%, based on the assets involved with these strategies. These fees were “easily half or even two-thirds of the normal asset management fee for an account,” said a former advisor.

Another former senior Wells Fargo strategist points out that an options strategy can make sense. For instance, if someone owns a significant amount of stock in one company, he or she may want to protect against a decline in that stock. “My problem was with the quota,” he says, because it encouraged advisors to implement an options strategy even when it didn’t make sense.

The alternative investments requirement looked to several advisors like it presented potential conflicts of interest, because it could result in additional revenue for the bank. According to Wells Fargo’s consent form, which it gave to clients to sign off on these investments, the bank may “receive compensation” that is “in addition to the fees that Wells Fargo receives for performing fiduciary services for your Account.”

The consent form acknowledges the conflict of interest potential directly: “Because of the compensation received by our affiliates in connection with the Fund, Wells Fargo’s investment of the Account in the Fund may be considered a conflict of interest.”

Wells Fargo says that in the majority of cases, rebates are passed down to clients.

“When fund managers provide a rebate of fund fees, Wells Fargo deposits the full rebate for our clients’ benefit,” says Leordeanu. “For a small number of certain funds, Wells Fargo may be compensated for services provided to the funds, as disclosed to and consented by clients prior to investment.”

With separately managed accounts, where the goal was “at least three new third party” accounts per advisor for 2016, there were also additional fees. Separately managed accounts carried expenses of 0.30-0.80% for equity strategies, according to various fee schedules.

“As part of our asset allocation strategy, we offer a variety of services to meet our clients’ financial needs and objectives in a properly risk adjusted portfolio and we have supervisory processes and controls in place,” says Erik Davidson, the chief investment officer of Wells Fargo Wealth Management. “Access to Private Placement investments, Separately Managed Accounts, and Options Strategies are among many of the benefits of being a client of Wells Fargo Private Bank. Wells Fargo investment professionals have a strong understanding of these investment solutions, which are intended to improve the risk-adjusted return outcomes of high net worth investors’ portfolios. We take seriously our responsibility to ensure that all of our Private Bank clients are informed and educated about the investment solutions that may be appropriate for their individual circumstances.”

In addition to extra fees and expenses for options, numerous fee schedules Yahoo Finance reviewed disclosed that the bank may charge brokerage commissions on top of the annual fee clients paid for portfolio management. Former advisors told Yahoo Finance that clients frequently complained about these additional fees. Most clients who pay an annual fee do not also pay trading commissions.

Yahoo Finance reviewed five client statements in which both commissions and assets-under-management–based fees were charged. The commissions added around single-digit basis points (between 0.04% and 0.09%) to the total amount the clients were paying, a former advisor said. Another former advisor said commissions could add up to 0.25% if there was 30% turnover of securities in a portfolio.

These fees were not kept by Wells Fargo; they were simply expenses for trading and research. However the norm for competitors of Wells Fargo’s Private Bank is to include commissions or trading expenses in the asset-based fee, according to sources across the financial industry with knowledge of the matter. Charging clients separately for the two types of fees would allow a bank to show clients a potentially lower and more competitive annual-fee figure against another bank’s commission-included fee.

Advisors faced pressure that could put client interests second

If advisors didn’t meet goals of certain amounts of options, separately managed accounts, and private placement alternatives in their book of clients, their bonuses were penalized, according to advisors and documents.

Performance review documents reviewed by Yahoo Finance showed advisors being evaluated on their “investment execution,” which was based on utilizing alternatives, options, and private placements, and praised for using options in client portfolios because it was a “significant driver of revenue.”

“All of a sudden if you’re not doing so many separately managed accounts, your bonus was reduced,” one advisor recalls.

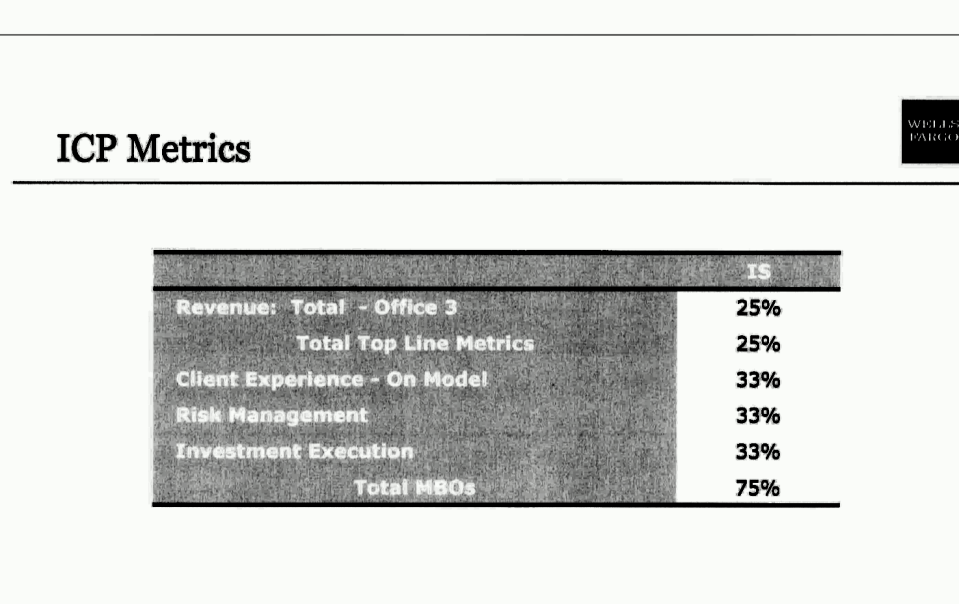

There was also a direct link between compensation and the overall fees an advisor generated. According to the “2017 WM Compensation Plan,” 25% of “incentive compensation plan managerial business objectives” or ICP MBO — which was internal language for sales goals — was based on fee revenue.

This could put advisors in tough situations, the advisor recalled, when they would be faced with the dilemma of putting a client in an investment that may not have been the best choice for them or risk their bonus.

“In all the different parts of our Wealth and Investment Management businesses — whether retail brokerage, trust, wealth or retirement — our team members are focused on our clients and their unique financial needs,” Leordeanu says. “While different types of accounts have different fees, all fees are fully disclosed. We are committed to transparency as we work with our clients to help them realize their financial goals.”

Indeed, Wells Fargo did not hide any of the fees. They were present in consent forms and fee schedules. However, clients were not given the “internal use only” documents demonstrating advisors’ incentives for their bonuses.

In some cases, clients were also not explicitly informed when additional fees present on the various fee schedules were activated. According to two former advisors at the Private Bank, many accounts were discretionarily managed, meaning client approval wasn’t required for each move.

“Where the managers went first was in the irrevocable trust, where Wells Fargo was trustee, where they can decide what to do,” one said. “That’s where all these strategies went first, and lots of them. Fees on fees.”

For advisors trying to meet a quota but lacking enough clients they felt could benefit from SMAs, irrevocable trusts were the easiest way to meet it.

Another advisor discussing the irrevocable trust fee schedule recalled hearing a manager say, “So long as you disclose it, you can charge it!”

Advisors were expected to sell

In addition to the use of advanced investing options, Wells Fargo advisors in the Private Bank were also required to generate other business in the form of loans, mortgages, and wealth-planning products, or, once again, put their bonuses in jeopardy.

According to former advisors and internal documents, those “ICP MBOs” were also tied to getting clients to deepen their connections with Wells Fargo.

Advisors were required to have “full outside line of business participation,” which meant that an advisor was obligated to bring on other Wells Fargo employees from other divisions like banking, brokerage, or planning. Since bonuses depended on this, advisors were incentivized to use such services whether the client needed it or not.

“Comp drives behavior,” said one former advisor. Performance review documents for advisors in the private bank show “execution of the Tactical Sales Process” as an area of evaluation.

Wells Fargo advisors were also incentivized to pitch other Wells Fargo products themselves, according to 2016 compensation plan documents for Private Bank advisors. For referring clients to mortgages, lines of credit, loans, and estate fees, advisors would receive fee credit that counted towards bonuses.

“Acknowledge the important support that Advisors provide on larger, more complex portfolio mortgages that are not sourced by an Advisor,” reads a document called “2017 WM Compensation Plan. “[This] is consistent with Wealth Management’s philosophy of rewarding sales and sourcing activity.”

This, the advisors said, was not always in the best interests of the client, something that conflicted with their responsibility as fee-compensated fiduciaries.

“You had to do so many mortgages. Two or three mortgage referrals every year — one or two had to stick,” the advisor said. “It only behooves us to find solutions, and you might as well find solutions in-house. But when it becomes your job to find those you neglect what your clients need.”

Turning to planning

Wells Fargo advisors were also instructed to get clients to do “Client Discovery Reviews,” or CDRs in Wells lingo. These were reviews conducted with clients that highlighted areas in which a client could use additional products or services. One former executive defends CDRs as a helpful tool, but others viewed them as a thinly veiled sales push.

According to internal presentation documents from the “Wealth Regional Development Conference 2015,” CDRs were introduced as a criteria for advisors’ bonuses that year.

“We show you CDR/Planning and Full Participation [as ‘key measurables’] because even the discretionary award criteria has an expectation around these,” the presentation documents read. Other internal documents, such as performance reviews, highlight “planning penetration” and “client discovery review” as “critical business metrics.”

While the CDR was free, it also opened the door to selling a client on a full financial plan, which was not free, or additional products. The fees for planning, according to an internal presentation called “The Wealth Planning Client Experience,” were significant: from $5,000 to $68,000 per year, depending on the client’s assets. The CDR “was the gateway for pitching the Planning Engagement,” said a former advisor. “It would also be used to tell the client they didn’t have enough life insurance or that maybe an annuity would be a good idea based on the need for more income in retirement.”

Advisors were also told they “should include a Planner” for client portfolios over $5 million, according to that internal presentation.

Wells Fargo’s motivation to increase CDRs and planning is made clear in the same document, which notes that the use of these tools results in “Deeper Cross-Sell” and “151% more revenue.”

“The Planners strive to convert each client into signing a planning engagement for 12 months during which they find other areas the client may have gaps where a product can be sold,” said one former advisor.

Three of the former Wells Fargo employees interviewed complained about the ethics of the planning engagement and a culture of pushing these planning solutions on clients. In one instance, a former employee recalled that before a sales meeting with a prospect, he said a proposed plan wasn’t in the best interest of a client. He was left off the call. A former colleague confirmed that this employee was eventually penalized for not selling enough.

“It was a very strong sales culture,” he said. “It was mostly growing your book of business. Get more assets under management. Write more loans.”

Another noted that advanced planning was only really necessary for clients with over $11 million, because of complexities of the estate tax.

Even as Wells Fargo’s public image took a beating, advisors were still being asked to look for opportunities to expand planning. On the day former CEO John Stumpf appeared in front of the Senate Banking Committee to answer for the bank’s retail banking sins, the then–senior director of sales Susan Mayo and senior director of planning Amy Theisen emailed the advisors to “reach out to every client in your book” to look for CDR opportunities.

“This is a great opportunity to highlight to your clients … that we lead with Discovery,” she wrote.

Of course, it made sense for Wells advisors to find a way to touch base with clients at such a precarious time. But one former advisor was horrified by the email, because he viewed it as a “thinly veiled sales push for the planning process — something that sounds good on paper as part of a client experience, but was nothing more than a tool to increase revenue on every client.” Indeed, if Wells truly wanted to change — and not just to advertise that it has changed — transparency about the ways employees are paid might be a way to start.

–

Read more:

Exclusive: Wells Fargo automated high-net-worth wealth management as advisors faced sales pressure

Every Wells Fargo consumer scandal since 2015: a timeline

Wells Fargo’s scandals just won’t die

Bethany McLean is a contributing editor at Vanity Fair and bestselling author. Her latest book, “Saudi America: The Truth About Fracking and How It’s Changing the World,” is coming out in September 2018.

Ethan Wolff-Mann is a senior writer at Yahoo Finance focusing on consumer issues, tech, and personal finance. Follow him on Twitter @ewolffmann. You can contact him at [email protected].