Exploring Three Swedish Exchange Stocks With Intrinsic Value Discounts Ranging From 13.9% To 35%

Amid a backdrop of fluctuating global markets, Sweden's stock exchange presents intriguing opportunities for investors seeking value. Recent trends indicate varying performances across sectors, with certain Swedish stocks appearing undervalued compared to their intrinsic worth. In this context, identifying stocks that are trading below their fundamental value could be particularly compelling, especially in a market environment where discerning undervaluation becomes both an art and a science.

Top 10 Undervalued Stocks Based On Cash Flows In Sweden

Name | Current Price | Fair Value (Est) | Discount (Est) |

Sleep Cycle (OM:SLEEP) | SEK40.90 | SEK74.28 | 44.9% |

Gr?nges (OM:GRNG) | SEK132.40 | SEK259.92 | 49.1% |

Husqvarna (OM:HUSQ B) | SEK72.50 | SEK142.26 | 49% |

Nordic Waterproofing Holding (OM:NWG) | SEK161.20 | SEK311.10 | 48.2% |

Volati (OM:VOLO) | SEK120.00 | SEK233.15 | 48.5% |

RaySearch Laboratories (OM:RAY B) | SEK140.60 | SEK277.84 | 49.4% |

TF Bank (OM:TFBANK) | SEK266.00 | SEK519.66 | 48.8% |

Nordisk Bergteknik (OM:NORB B) | SEK17.00 | SEK30.99 | 45.1% |

Sinch (OM:SINCH) | SEK28.54 | SEK56.74 | 49.7% |

Bactiguard Holding (OM:BACTI B) | SEK70.80 | SEK133.56 | 47% |

Below we spotlight a couple of our favorites from our exclusive screener.

Fortnox

Overview: Fortnox AB operates in providing financial and administrative software solutions to small and medium-sized businesses, accounting firms, and organizations, with a market capitalization of approximately SEK 40.14 billion.

Operations: Fortnox's revenue is primarily derived from core products (SEK 734 million), followed by businesses (SEK 378 million), accounting firms (SEK 352 million), financial services (SEK 249 million), and marketplaces (SEK 160 million).

Estimated Discount To Fair Value: 13.9%

Fortnox, a Swedish software company, has shown robust financial performance with its latest earnings report highlighting a substantial increase in sales and net income. The company's revenue and profit growth are outpacing the broader Swedish market, with projections indicating continued strong growth rates. Despite this positive outlook, Fortnox is currently trading at 13.9% below our estimated fair value of SEK 76.45, suggesting it may be undervalued based on discounted cash flow analysis. However, its forecasted revenue growth is slightly below the significant threshold of 20% per year.

Nolato

Overview: Nolato AB operates in the development, manufacturing, and sale of plastic, silicone, and thermoplastic elastomer products across various sectors including medical technology, pharmaceuticals, consumer electronics, and automotive, with a market capitalization of SEK 15.56 billion.

Operations: The Medical Solutions segment generates SEK 5.34 billion in revenue.

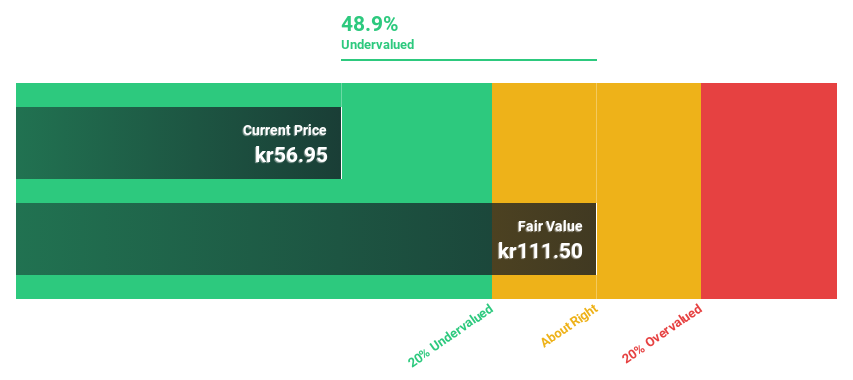

Estimated Discount To Fair Value: 35%

Nolato has demonstrated a consistent increase in earnings and sales, reflecting a promising growth trajectory that exceeds the broader Swedish market's average. Despite an unstable dividend history, the company is trading at a significant 35% discount to its estimated fair value of SEK 88.91, suggesting potential undervaluation based on cash flows. However, its expected return on equity is projected to be modest in three years at 14.6%, which may temper investor expectations regarding long-term profitability.

The analysis detailed in our Nolato growth report hints at robust future financial performance.

Take a closer look at Nolato's balance sheet health here in our report.

Sweco

Overview: Sweco AB (publ) offers architecture and engineering consultancy services globally, with a market capitalization of approximately SEK 61.05 billion.

Operations: Sweco's revenue is generated from various regional segments, with Sweden contributing SEK 8.74 billion, followed by Belgium at SEK 3.97 billion, Norway at SEK 3.50 billion, Finland at SEK 3.67 billion, Denmark at SEK 3.24 billion, the Netherlands at SEK 3.00 billion, and Germany & Central Europe providing SEK 2.71 billion.

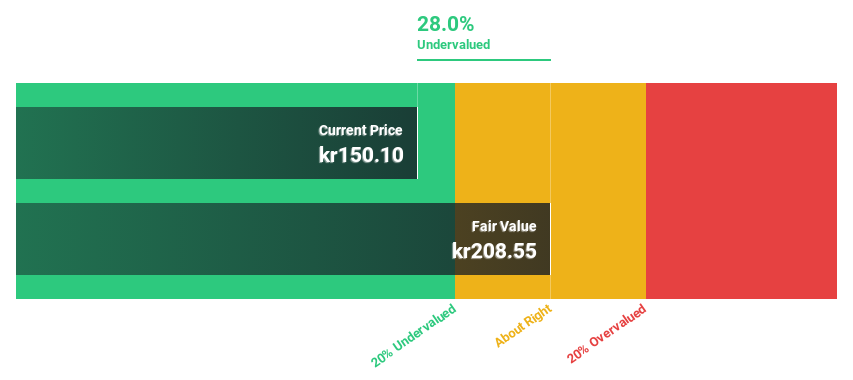

Estimated Discount To Fair Value: 17.4%

Sweco AB, with its shares priced at SEK 169.8—17.4% below the calculated fair value of SEK 205.46—appears undervalued based on discounted cash flows. The company's earnings have grown by 1.2% over the past year and are expected to increase by 17.31% annually, outpacing the Swedish market's growth rate of 15.5%. Despite this positive trajectory, Sweco has a history of unstable dividend payments, which could concern income-focused investors.

The growth report we've compiled suggests that Sweco's future prospects could be on the up.

Click to explore a detailed breakdown of our findings in Sweco's balance sheet health report.

Seize The Opportunity

Reveal the 51 hidden gems among our Undervalued Swedish Stocks Based On Cash Flows screener with a single click here.

Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Looking For Alternative Opportunities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include OM:FNOX OM:NOLA B and OM:SWEC B.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]