Yahoo Finance

Yahoo Finance Exploring Undervalued Opportunities On SEHK With Discounts Ranging From 41% To 48.8%

Amidst a backdrop of global economic uncertainties and fluctuating markets, the Hong Kong stock market has recently shown signs of undervaluation, presenting potential opportunities for investors. Given the current market conditions where value stocks are gaining interest, exploring undervalued stocks on the SEHK could be a prudent strategy for those looking to capitalize on discounts ranging from 41% to 48.8%.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

Name | Current Price | Fair Value (Est) | Discount (Est) |

Giant Biogene Holding (SEHK:2367) | HK$39.65 | HK$76.17 | 47.9% |

Beauty Farm Medical and Health Industry (SEHK:2373) | HK$17.50 | HK$33.17 | 47.2% |

Bairong (SEHK:6608) | HK$8.70 | HK$15.62 | 44.3% |

AIA Group (SEHK:1299) | HK$50.85 | HK$88.64 | 42.6% |

Shanghai INT Medical Instruments (SEHK:1501) | HK$27.85 | HK$48.46 | 42.5% |

Hangzhou SF Intra-city Industrial (SEHK:9699) | HK$10.12 | HK$19.64 | 48.5% |

FIT Hon Teng (SEHK:6088) | HK$2.63 | HK$4.54 | 42% |

AK Medical Holdings (SEHK:1789) | HK$4.41 | HK$7.99 | 44.8% |

Vobile Group (SEHK:3738) | HK$1.18 | HK$2.30 | 48.8% |

MicroPort Scientific (SEHK:853) | HK$5.09 | HK$9.42 | 46% |

Let's review some notable picks from our screened stocks.

Best Pacific International Holdings

Overview: Best Pacific International Holdings Limited specializes in manufacturing, trading, and selling elastic fabric, elastic webbing, and lace, with a market capitalization of approximately HK$2.35 billion.

Operations: The company generates revenue primarily through two segments: HK$834.34 million from the production and sale of elastic webbing, and HK$3.37 billion from the production and sale of elastic fabric and lace.

Estimated Discount To Fair Value: 41%

Best Pacific International Holdings, priced at HK$2.25, is significantly undervalued based on DCF analysis, with an estimated fair value of HK$3.81. The company’s earnings have grown by 15.9% over the past year and are expected to increase by 24.29% annually over the next three years, outpacing Hong Kong's market growth rate of 11.3%. Despite its unstable dividend track record and a recent cautious approach from international customers impacting sales, Best Pacific anticipates a substantial net profit of not less than HK$260 million for HY 2024, nearly doubling the previous year's figure due to improved confidence in economic recovery and increased customer restocking.

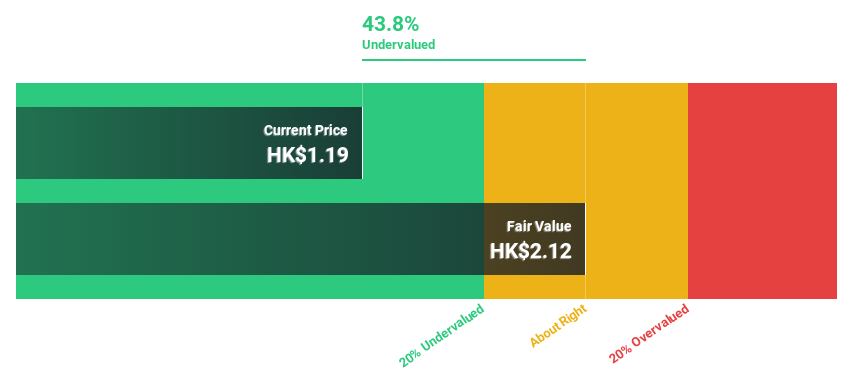

Vobile Group

Overview: Vobile Group Limited, an investment holding company, offers software as a service for digital content asset protection and transactions across the United States, Japan, Mainland China, and other international markets with a market capitalization of approximately HK$2.69 billion.

Operations: The company generates revenue primarily through its SaaS offerings, totaling approximately HK$2.00 billion.

Estimated Discount To Fair Value: 48.8%

Vobile Group, with a current trading price of HK$1.18, is perceived as undervalued based on DCF analysis, indicating a fair value of HK$2.3. Despite low forecasted ROE at 6.6% in three years, the company's earnings are expected to surge by 66.63% annually. Revenue growth projections stand at 21.7% per year, surpassing Hong Kong’s average market growth rate of 7.7%. However, shareholder dilution has occurred over the past year which might raise concerns among investors about future equity value erosion.

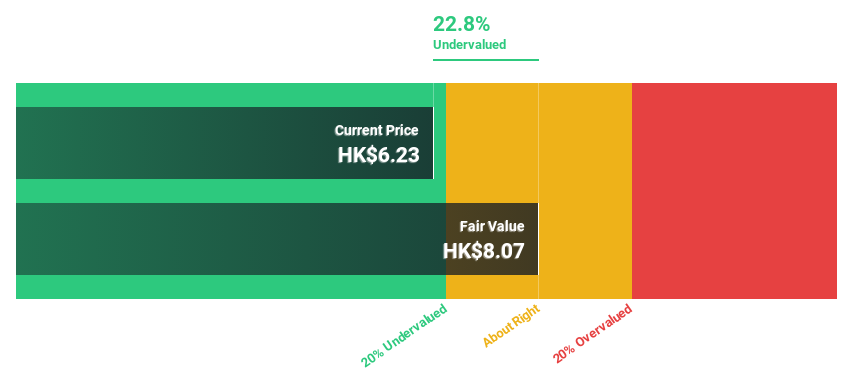

MicroPort Scientific

Overview: MicroPort Scientific Corporation is an investment holding company that manufactures and markets medical devices across regions including the People’s Republic of China, North America, Europe, and South America, with a market capitalization of approximately HK$9.29 billion.

Operations: MicroPort Scientific's revenue is generated from various segments including Orthopedics Devices at $238.37 million, Neurovascular Devices at $94.17 million, Cardiac Rhythm Management (CRM) at $207.04 million, Endovascular and Peripheral Vascular Devices at $168.22 million, Cardiovascular Devices (excluding CRM & Surgical Robot Device & Heart Valve Business) at $158.88 million, Heart Valve Business at $47.52 million, Surgical Robot Devices Business at $14.81 million, and Surgical Devices Business at $7.76 million.

Estimated Discount To Fair Value: 46%

MicroPort Scientific, priced at HK$5.09, is trading well below its estimated fair value of HK$9.42, reflecting a significant undervaluation based on DCF analysis. The company is expected to become profitable within the next three years with an earnings growth forecast of 74.27% per year. Although its revenue growth at 14.7% annually is slower than some high-growth benchmarks, it still outpaces the average market rate in Hong Kong (7.7%). Recent board changes and corporate governance updates could influence strategic directions ahead.

Turning Ideas Into Actions

Gain an insight into the universe of 38 Undervalued SEHK Stocks Based On Cash Flows by clicking here.

Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Want To Explore Some Alternatives?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SEHK:2111 SEHK:3738 and SEHK:853.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]