Exploring Undervalued Small Caps With Insider Action In Australia July 2024

In the past week, Australia's market has experienced a slight downturn with a 1.2% drop, yet it maintains a robust annual growth of 7.8%, with earnings expected to grow by 13% annually. In this context, undervalued small-cap stocks showing insider buying activity could present intriguing opportunities for investors looking to capitalize on potential market inefficiencies and anticipated growth.

Top 10 Undervalued Small Caps With Insider Buying In Australia

Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

Neuren Pharmaceuticals | 16.4x | 11.1x | 49.13% | ★★★★★☆ |

Healius | NA | 0.6x | 41.95% | ★★★★★☆ |

Dicker Data | 21.4x | 0.8x | 3.31% | ★★★★☆☆ |

Eagers Automotive | 9.5x | 0.3x | 34.85% | ★★★★☆☆ |

Elders | 22.9x | 0.5x | 43.31% | ★★★★☆☆ |

Codan | 30.3x | 4.4x | 24.46% | ★★★★☆☆ |

Smartgroup | 17.4x | 4.3x | 49.65% | ★★★☆☆☆ |

Gold Road Resources | 16.6x | 4.1x | 46.82% | ★★★☆☆☆ |

Coventry Group | 297.7x | 0.5x | -11.53% | ★★★☆☆☆ |

RAM Essential Services Property Fund | NA | 6.0x | 36.41% | ★★★☆☆☆ |

Let's uncover some gems from our specialized screener.

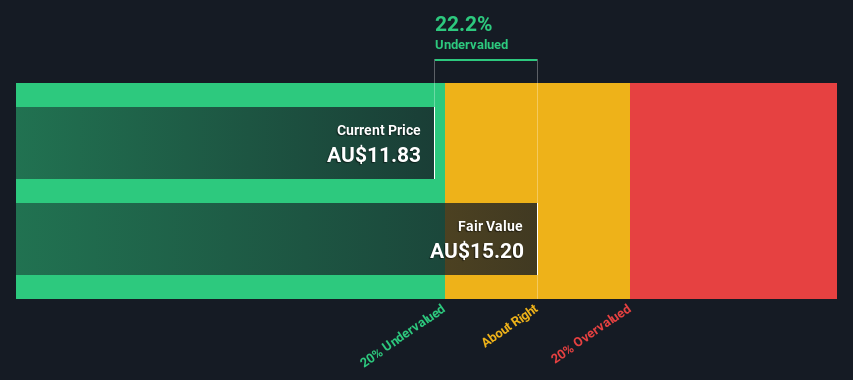

Codan

Simply Wall St Value Rating: ★★★★☆☆

Overview: Codan is a diversified technology company that specializes in communications, metal detection, and other electronic technologies, with a market capitalization of approximately A$1.31 billion.

Operations: The company generates revenue primarily from Communications and Metal Detection, contributing A$291.50 million and A$212.20 million respectively. Gross profit margin has shown a trend, fluctuating between 54% to 57% over recent periods, reflecting variability in cost management relative to sales.

PE: 30.3x

Recently, Codan has demonstrated a compelling financial trajectory with earnings expected to grow by 16.2% annually. Despite the reliance on external borrowing—posing a higher risk due to the absence of customer deposits—the company continues to attract insider confidence, evidenced by their recent share purchases. This activity underscores a strong belief in Codan's prospects among those closest to its operations, reinforcing its appeal in the context of undervalued entities within Australia’s vibrant market landscape.

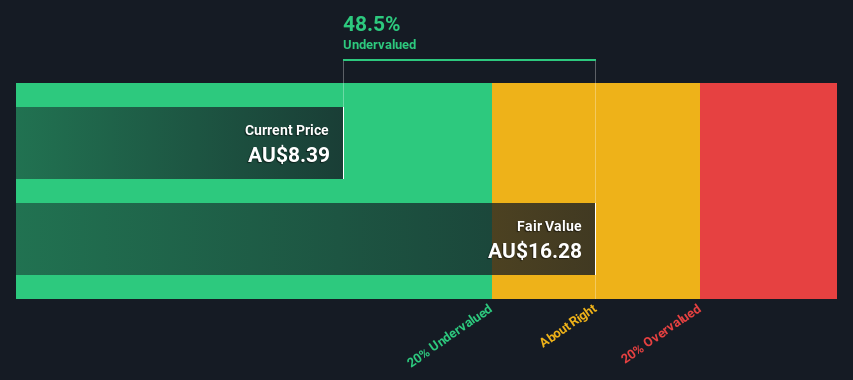

Elders

Simply Wall St Value Rating: ★★★★☆☆

Overview: Elders is an Australian company involved in providing a range of services including branch network operations, wholesale products, feed and processing services, and corporate services.

Operations: Branch Network generates the largest portion of revenue at A$2.54 billion, followed by Wholesale Products and Feed and Processing Services, which contribute A$341.19 million and A$120.14 million respectively. The gross profit margin has shown a fluctuating trend over recent periods, with the latest recorded at 19.41%.

PE: 22.9x

Elders, a notable player in the Australian market, has recently been marked by significant insider confidence, with key purchases underscoring a strong belief in its future. Despite a challenging half year ending March 2024, where net sales dropped to A$1.34 billion and net income fell to A$11.59 million, the company's leadership remains optimistic. With earnings expected to rise by nearly 23% annually and Glenn Davis joining as a director later this year, Elders is poised for recovery and growth.

Navigate through the intricacies of Elders with our comprehensive valuation report here.

Evaluate Elders' historical performance by accessing our past performance report.

NRW Holdings

Simply Wall St Value Rating: ★★★☆☆☆

Overview: NRW Holdings is a diversified provider of mining and civil construction services with a market capitalization of approximately A$1.76 billion.

Operations: The gross profit margin of the company has shown a fluctuating trend over the years, ranging from 41.30% to 62.52%, reflecting variations in cost management and revenue generation efficiency across different periods. With significant contributions from its three main segments—Mining (A$1.49 billion), MET (A$739.07 million), and Civil (A$593.62 million)—the company has navigated through diverse market conditions without relying on any "Other," "Unallocated," or "Inter-Segment" financial inputs in its reporting structure.

PE: 17.3x

With a reaffirmed revenue forecast of A$2.9 billion for 2024, NRW Holdings Limited recently showcased robust financial health, further bolstered by a successful equity offering raising A$5.26 million at A$2.56 per share. Insider confidence is evident as they recently purchased shares, signaling trust in the company's prospects amidst external borrowing as its sole funding source—considered riskier but manageable given the firm's growth trajectory with earnings expected to rise by 13.33% annually. This paints NRW Holdings as an appealing choice within Australia’s undervalued sectors, poised for potential growth.

Get an in-depth perspective on NRW Holdings' performance by reading our valuation report here.

Assess NRW Holdings' past performance with our detailed historical performance reports.

Key Takeaways

Get an in-depth perspective on all 19 Undervalued ASX Small Caps With Insider Buying by using our screener here.

Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready To Venture Into Other Investment Styles?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ASX:CDA ASX:ELD and ASX:NWH.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]