The central bank’s unprecedented strategy of unwinding its balance sheet is quickly coming into focus as worried investors urge the Fed to pause its rate hikes.

The main concern: a reversal of the Fed’s massive holdings of U.S. Treasurys and mortgage-backed securities — accumulated during seven years of quantitative easing — could pull liquidity from an economy already at risk of recession. As part of the “quantitative tightening” process, those assets will reach maturity without being replaced, essentially running off the balance sheet and shrinking the pool of securities that exist in the market.

President Donald Trump is the latest figure publicly calling on the Fed to pump the brakes on its tightening policy, citing the Wall Street Journal editorial board in urging the Fed not to “let the market become any more illiquid than it already is.”

I hope the people over at the Fed will read today’s Wall Street Journal Editorial before they make yet another mistake. Also, don’t let the market become any more illiquid than it already is. Stop with the 50 B’s. Feel the market, don’t just go by meaningless numbers. Good luck!

— Donald J. Trump (@realDonaldTrump) December 18, 2018

Some are sounding the alarm but others say there’s no need to panic.

Not all ‘rainbows and unicorns’

Trump’s comments come after this weekend’s Wall Street Journal opinion piece from investor Stan Druckenmiller and former Fed Governor Kevin Warsh. The two warned that in conjunction with raising rates, the Fed’s balance sheet unwind creates a “double-barreled blitz” of policy impediments that could threaten a U.S. economy still capable of growth. Their recommendation: cancel the December rate hike, as others have suggested.

“We were assured by policy makers that QE provided large benefits to the real economy. If so, won’t its reversal in the form of QT come with a cost?” the two wrote. “It can’t be all rainbows and unicorns.”

Nomura also raised red flags on the QT process, adding that liquidity is an international concern since other central banks are also expected to tighten their QE programs. On Thursday, the European Central Bank formally ended its bond purchase program.

“It’s easy to paint a picture of a market crisis in 2019, market liquidity conditions worsening with lingering effects of Fed hikes and continued balance reduction,” Nomura wrote in a note Dec. 11.

If the “50 B’s” in Trump’s tweet is referring to the $50 billion of monthly asset run-offs, the president appears to be making the case for the Fed to halt its balance sheet unwind process entirely. But by design, the Fed’s drawdown functions on “autopilot” and the Fed has said it would only resume asset purchases if there were a “sufficient” negative shock to the economy.

Still plenty of liquid

Richard Bernstein, head of Richard Bernstein Advisors LLC, acknowledged that liquidity is “drying up” but said it’s normal for central banks to remove liquidity from an economy in the late stages of a business cycle. So why the increased volatility and market sell-off? Bernstein said Fed actions tend to lag the data (as opposed to lead it), meaning that it is natural economic forces at work and not a Fed-included liquidity crunch.

“Blaming the Fed for the markets’ ongoing volatility seems convenient but unjustified,” Bernstein said.

Brian Rehling, co-head of global fixed income strategy at the Wells Fargo Investment Institute, is also hesitant to sound the alarm on liquidity, arguing that the Fed is only in the early stages of normalization and is leaving “plenty of money” in the system.

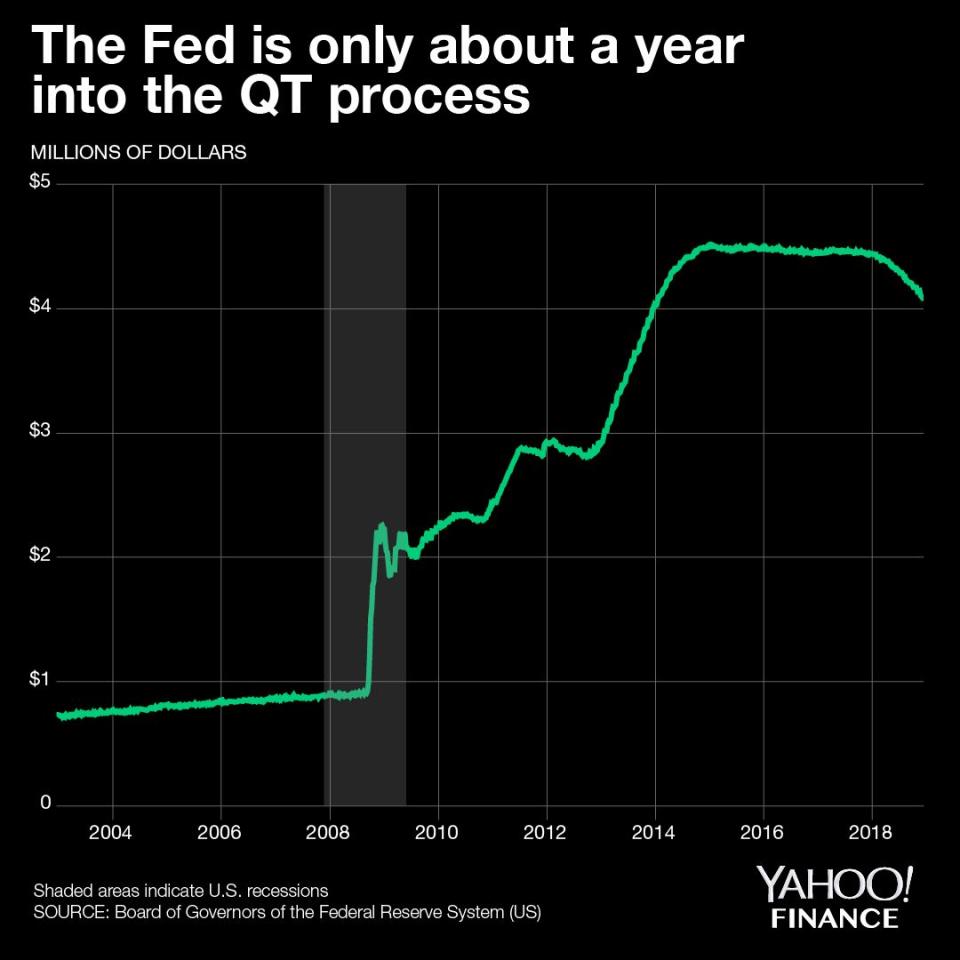

Even though the Fed has shed over $370 billion in assets since starting the great unwind, the balance sheet still sits at a gargantuan $4.0 trillion. And while the Fed is still mum on exactly when it will stop the QT process, most market analysts expect the central bank to draw down its balance sheet to a target level that is still well above pre-crisis levels.

But Rehling told Yahoo Finance that markets should still pay attention; he said he expects the Fed to share more detail on how large it would like its ideal balance sheet and when it expects to get there.

“It’s something to watch out for later this year,” Rehling said.

Other analysts have already published guesses on the Fed’s target balance sheet size; Goldman Sachs estimates $3.6 trillion and UBS projects $3.5 trillion.

Until the Fed shares more detail, it’s anyone’s guess as to how large the balance sheet will end up.

Brian Cheung is a reporter covering the banking industry and the intersection of finance and policy for Yahoo Finance. You can follow him on Twitter @bcheungz.

Read more:

Why 2019 could be the year of the big bank merger

Congress may have accidentally freed nearly all banks from the Volcker Rule

NY Fed’s Williams: There’s still room for ‘further gradual’ rate increases

FDIC chair: We need to be preparing for the next downturn

Atlanta Fed’s Bostic joins chorus of concern over leveraged lending