MicroPort CardioFlow Medtech And Two Other SEHK Stocks That May Be Priced Below Their Estimated True Value

Amidst a global landscape of shifting economic indicators and market reactions, the Hong Kong stock market presents unique opportunities for discerning investors. As inflationary pressures and policy responses shape markets worldwide, identifying undervalued stocks in Hong Kong could offer potential value in an environment ripe with cautious optimism.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

Name | Current Price | Fair Value (Est) | Discount (Est) |

Giant Biogene Holding (SEHK:2367) | HK$41.60 | HK$75.36 | 44.8% |

China Cinda Asset Management (SEHK:1359) | HK$0.68 | HK$1.29 | 47.4% |

China Resources Mixc Lifestyle Services (SEHK:1209) | HK$25.80 | HK$48.19 | 46.5% |

West China Cement (SEHK:2233) | HK$1.08 | HK$2.16 | 49.9% |

BYD (SEHK:1211) | HK$246.60 | HK$461.90 | 46.6% |

Zijin Mining Group (SEHK:2899) | HK$17.58 | HK$32.24 | 45.5% |

Super Hi International Holding (SEHK:9658) | HK$14.44 | HK$26.10 | 44.7% |

Melco International Development (SEHK:200) | HK$5.28 | HK$10.40 | 49.2% |

Vobile Group (SEHK:3738) | HK$1.28 | HK$2.33 | 45% |

Zylox-Tonbridge Medical Technology (SEHK:2190) | HK$11.18 | HK$22.03 | 49.3% |

Let's explore several standout options from the results in the screener.

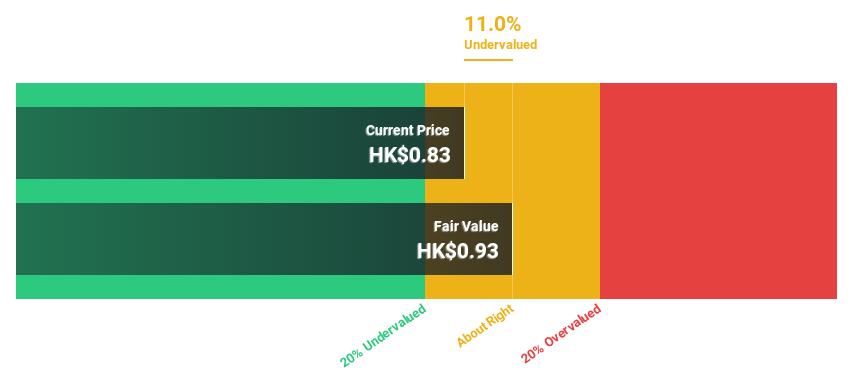

MicroPort CardioFlow Medtech

Overview: MicroPort CardioFlow Medtech Corporation is a medical device company focused on developing and commercializing transcatheter and surgical solutions for structural heart diseases, operating both in the People’s Republic of China and internationally, with a market capitalization of approximately HK$2.15 billion.

Operations: The company generates revenue primarily from its Surgical & Medical Devices segment, amounting to CN¥336.22 million.

Estimated Discount To Fair Value: 24.2%

MicroPort CardioFlow Medtech is positioned as an undervalued stock based on cash flows, trading at HK$0.89 against a fair value of HK$1.17, reflecting a 24.2% discount. The company's rapid revenue growth forecast at 21.4% annually surpasses the Hong Kong market average significantly. Despite a low projected return on equity of 4%, profitability is expected within three years with earnings potentially increasing by approximately 98.57% annually. Recent corporate guidance anticipates a revenue rise between 22%-28%, driven by expanding hospital reach and new product commercializations in China and abroad, enhancing its investment appeal despite some financial softness in equity returns.

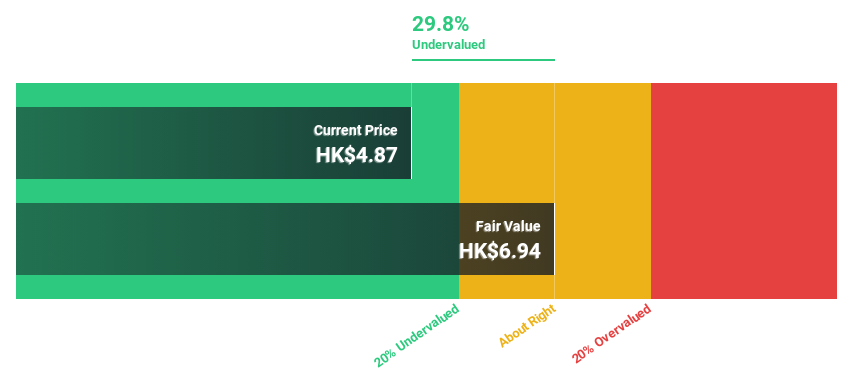

Zylox-Tonbridge Medical Technology

Overview: Zylox-Tonbridge Medical Technology Co., Ltd. is a medical device company specializing in neuro- and peripheral-vascular interventional devices, operating both in the People’s Republic of China and internationally, with a market capitalization of approximately HK$3.62 billion.

Operations: The company generates revenue primarily through the sale of neurovascular and peripheral-vascular interventional surgical devices, totaling CN¥527.75 million.

Estimated Discount To Fair Value: 49.3%

Zylox-Tonbridge Medical Technology, valued at HK$11.18, is significantly undervalued with its price 49.3% below the estimated fair value of HK$22.03 and more than 20% under DCF valuation. Anticipated to become profitable within three years, the company's revenue growth is projected at an impressive 24.1% annually, outpacing the Hong Kong market forecast of 7.7%. However, its forecasted Return on Equity remains low at 7.6%, suggesting potential challenges in achieving higher profitability efficiencies despite robust sales growth expectations and recent product approvals enhancing its market presence.

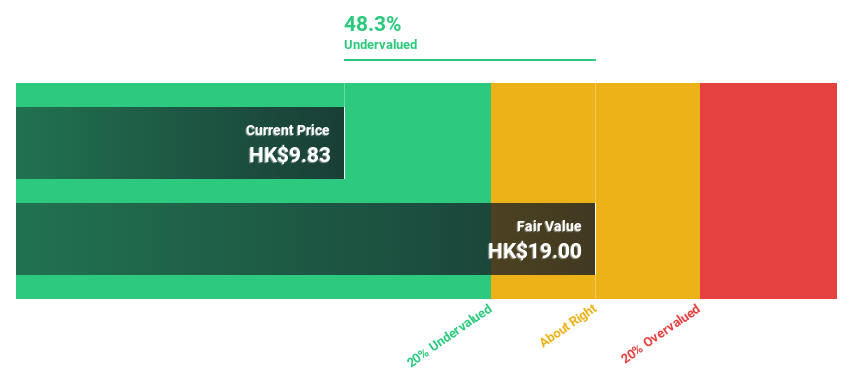

Bosideng International Holdings

Overview: Bosideng International Holdings Limited operates in the People’s Republic of China, focusing on the research, design, development, manufacturing, marketing, and distribution of branded down apparel and non-down products, as well as original equipment manufacturing (OEM) products; it has a market capitalization of approximately HK$45.72 billion.

Operations: Bosideng International Holdings primarily generates revenue through its down apparels segment, which brought in CN¥19.54 billion, supplemented by its original equipment manufacturing (OEM) management with CN¥2.70 billion, and smaller contributions from ladieswear and diversified apparels totaling approximately CN¥1.06 billion combined.

Estimated Discount To Fair Value: 30.2%

Bosideng International Holdings Limited, trading at HK$4.18, is perceived as undervalued based on DCF analysis, with its price 30.2% below the estimated fair value of HK$5.99. Recently reporting a robust earnings increase to CNY 3,074.07 million from CNY 2,138.57 million year-over-year and proposing a final dividend of HKD 0.20 per share reflects positive financial health but comes with an unstable dividend track record. Analysts expect both revenue and earnings to grow faster than the market average, although significant insider selling raises caution flags.

Key Takeaways

Unlock our comprehensive list of 44 Undervalued SEHK Stocks Based On Cash Flows by clicking here.

Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SEHK:2160 SEHK:2190 and SEHK:3998.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]