The R word has gotten popular, and there’s one new reason to fear the onset of a recession: a technical indicator known as the yield curve has crossed a threshold that often signals a downturn is coming.

That’s one factor in a sharp stock selloff on Dec. 4, with the S&P 500 off an alarming 3.2% and the NASDAQ down 3.8%. Other factors contributing to the selloff: confusion involving President Trump’s trade dispute with China, a slowdown in the housing market and general fears about declining profit margins.

The stock market has been choppy since the end of the summer, with the S&P 500 entering a technical correction—falling 10% from the prior peak—in late October. For the year, it’s basically flat, which is weak considering sharp cuts in corporate tax rates have sent profits soaring this year. Without the tax cuts, the market would probably be down for the first full year since the meltdown year of 2008.

[Check out our next-recession survival guide.]

Wall Street has suddenly begun chattering about a yield curve inversion, which happens when long-term interest rates—typically, Treasuries—fall below short-term rates. Interest rates are largely driven by market conditions, and long-term rates are normally higher because the risk of holding the debt over a long period of time is greater than the risk for short-term debt. But when long-term rates fall below short-term rates, that suggests borrowers expect a weak economy over the longer term, and usually, they’re right: a yield curve inversion has preceded every recession since 1957.

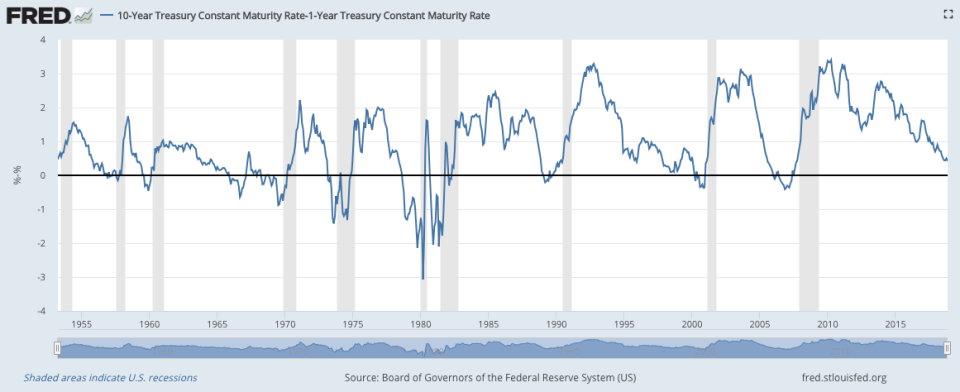

This chart shows the difference between rates on 10-year Treasuries and 1-year Treasuries, with the shaded areas indicating recessions. When the difference is less than 0, that means short-term rates are higher and the yield curve is inverted.

Long- and short-term rates have been converging this fall, with the curve flattening, as the chart above shows. Then, on Dec. 3, the interest rate on 5-year Treasuries fell below the rate on 2- and 3-year Treasuries. Yield curves can be computed using many different types of notes, and the usual benchmark compares 10-year Treasury rates with 3-month, 1-year or 2-year Treasuries. The differences in those long- and short-term rates are still positive. So the most reliable version of the yield curve still isn’t heralding a recession.

Plus, an inverted yield curve can be a false alarm. The difference between 10-year and 1-year Treasury rates went negative in 1966, but no recession ensued. The curve became positive again in 1967. It inverted again in 1969, and that time, the warning was real: a recession began in December of that year.

The yield curve has almost no effect on the ordinary lives of working people, and that’s a good thing. There are times when the stock market disconnects from the underlying economy, and this is probably one of them.

The real economy remains strong, with a very low unemployment rate, rising wages and above-average business and consumer optimism. Businesses are still hiring and many say they can’t find enough workers. Holiday shopping looks strong, a sign consumers are comfortable spending. President Trump’s grade on the Yahoo Finance Trumponomics Report Card is a B+, with the only notable weak spot being exports.

What economists worry about

What worries economists is mostly timing. The current economic expansion, which began in 2009, is in its 10th year, making it the second-longest upturn on record. By next summer, it will be the longest, surpassing the expansion that ran from 1991 to 2001. As economies expand, a gathering of forces typically creates conditions for the next recession, as rising wages push up prices and inflation, and various excesses develop. The Federal Reserve pushes back against inflation by raising interest rates—as it is doing now—but that in itself can crimp spending and contribute to a recession.

The probability of a recession 12 months from now is only around 14%, according to the New York Federal Reserve. Many economists think it’s lower. But economists do predict a slowdown in the growth rate of the U.S. economy. Forecasting firm Moody’s Analytics predicts real GDP growth will be 2.9% in 2018 and 2019, then fall to 0.9% in 2020. Economists sometimes call such a slowdown a “growth recession,” and it might compel companies to slow hiring and investment, as they wait to see if a real recession—defined as a contracting economy—develops. But a growth recession doesn’t typically come with huge layoffs and other scary moves that typify a real recession.

It’s still prudent for consumers to be cautious. Something unforeseen could cause a recession sooner than expected. President Trump’s protectionist trade policies are disrupting commerce, raising costs for businesses and worrying CEOs who are otherwise optimistic. If Trump miscalculates and presses too hard on tariffs or other protections, it could hurt the economy more than expected.

The next recession, when it does arrive, will also be harsh on some workers and probably kill some occupations for good. Companies often use recessions to remake their workforce, doing away with the least productive jobs and installing labor-saving technology where it makes sense. That means now is a good time to seek training, get new skills and prepare for the jobs that will exist after the next recession. Saving money is always a good idea, as is paying down debt and paring costs wherever possible. You may not need to do that urgently, but the more practice you have for the next recession, the better off you’ll be.

Confidential tip line: [email protected]. Click here to get Rick’s stories by email.

Read more:

Rick Newman is the author of four books, including “Rebounders: How Winners Pivot from Setback to Success.” Follow him on Twitter: @rickjnewman