SEHK Growth Companies With High Insider Ownership For July 2024

As global markets navigate through varying economic signals, with some regions showing signs of cooling while others maintain growth, the Hong Kong market has demonstrated resilience. In this context, exploring growth companies with high insider ownership in Hong Kong could offer unique insights into firms that potentially have a strong alignment between management’s interests and those of shareholders, especially valuable in these fluctuating market conditions.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

Name | Insider Ownership | Earnings Growth |

iDreamSky Technology Holdings (SEHK:1119) | 20.2% | 104.1% |

Pacific Textiles Holdings (SEHK:1382) | 11.2% | 37.7% |

Fenbi (SEHK:2469) | 32.8% | 43% |

Tian Tu Capital (SEHK:1973) | 34% | 70.5% |

Adicon Holdings (SEHK:9860) | 22.4% | 28.3% |

Zhejiang Leapmotor Technology (SEHK:9863) | 15% | 73.4% |

Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.7% | 79.3% |

Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 13.9% | 100.1% |

Ocumension Therapeutics (SEHK:1477) | 23.1% | 93.7% |

Beijing Airdoc Technology (SEHK:2251) | 28.7% | 83.9% |

Here we highlight a subset of our preferred stocks from the screener.

LifeTech Scientific

Simply Wall St Growth Rating: ★★★★☆☆

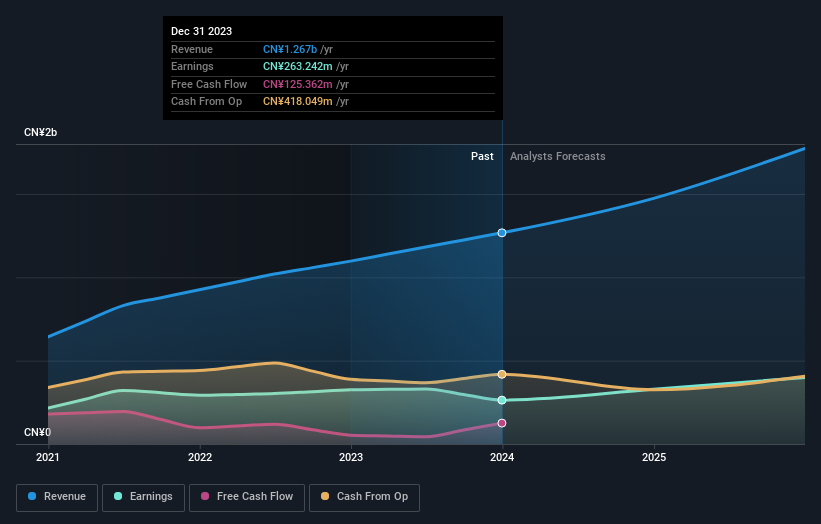

Overview: LifeTech Scientific Corporation, primarily engaged in developing, manufacturing, and trading interventional medical devices for cardiovascular and peripheral vascular diseases globally, has a market capitalization of approximately HK$6.48 billion.

Operations: The company generates revenue primarily from three segments: Structural Heart Diseases Business (CN¥495.67 million), Peripheral Vascular Diseases Business (CN¥707.11 million), and Cardiac Pacing and Electrophysiology Business (CN¥64.40 million).

Insider Ownership: 16%

LifeTech Scientific, a growth-oriented company in Hong Kong with significant insider ownership, has shown promising developments. Recent successful Phase II clinical study results of its IBS? Coronary Scaffold indicate comparable safety and effectiveness to existing stents, positioning it well for EU market entry. Despite high insider transactions recently favoring purchases, projected earnings growth at 20.55% annually outpaces the local market's 11.3%. However, revenue growth forecasts of 16.8% yearly lag behind the desired 20% threshold for high-growth entities, and a low forecasted Return on Equity (10.8%) could be a concern for future profitability metrics.

Dive into the specifics of LifeTech Scientific here with our thorough growth forecast report.

Our valuation report here indicates LifeTech Scientific may be overvalued.

SSY Group

Simply Wall St Growth Rating: ★★★★☆☆

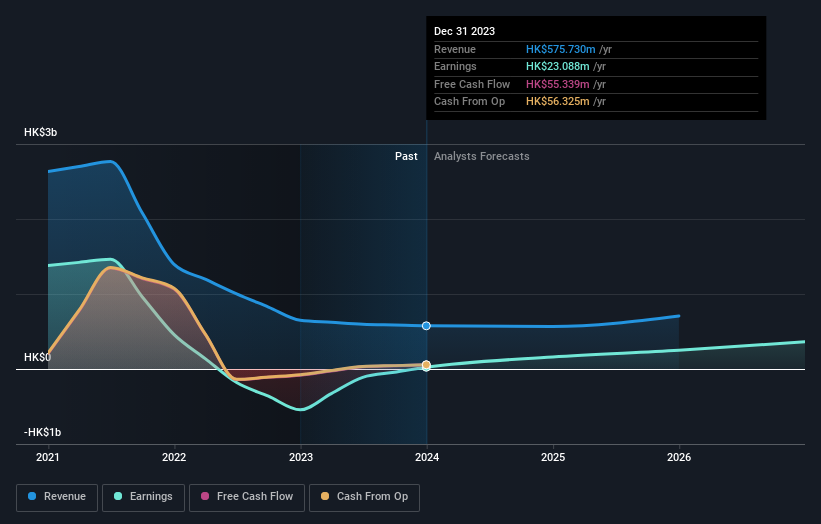

Overview: SSY Group Limited operates as an investment holding company that focuses on researching, developing, manufacturing, and selling a range of pharmaceutical products to hospitals and distributors in the People's Republic of China and globally, with a market capitalization of approximately HK$12.62 billion.

Operations: The company generates revenue primarily from two segments: Medical Materials, which brought in HK$0.39 billion, and Intravenous Infusion Solution and Others, which accounted for HK$6.30 billion.

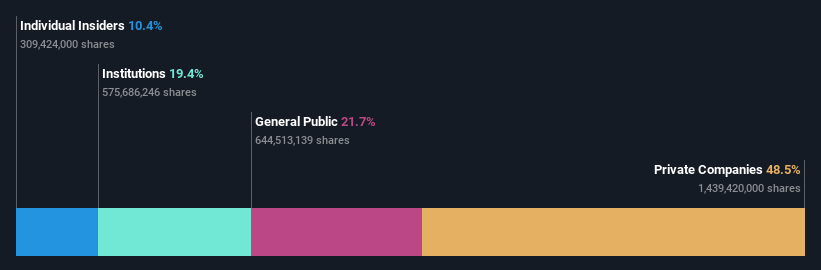

Insider Ownership: 10.4%

SSY Group, a Hong Kong-based company with high insider ownership, recently secured multiple product approvals from China's National Medical Products Administration, enhancing its market presence in pharmaceuticals. These approvals span a range of treatments including cardiovascular and neurological conditions, potentially boosting the company's growth trajectory. Despite this progress and a forecasted earnings growth of 15.03% per year, SSY’s revenue growth is expected to be moderate at 14% annually. Additionally, the dividend coverage by free cash flows appears weak.

Get an in-depth perspective on SSY Group's performance by reading our analyst estimates report here.

Value Partners Group

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Value Partners Group Limited, a publicly owned investment manager, operates with a market capitalization of approximately HK$2.81 billion.

Operations: The firm generates its revenue primarily from its asset management business, which accounted for HK$575.73 million.

Insider Ownership: 23.7%

Value Partners Group, a Hong Kong-based asset management firm, has recently experienced significant executive changes with the departure of CEO Ms. Wong and the appointment of Mr. Till Rosar as an independent non-executive director. Despite these transitions, the company is poised for notable growth with earnings expected to increase by 55.92% annually, outpacing the Hong Kong market's forecast of 11.3%. However, its revenue growth projection at 10.7% annually is modest compared to its earnings surge and below high-growth benchmarks.

Our expertly prepared valuation report Value Partners Group implies its share price may be too high.

Turning Ideas Into Actions

Navigate through the entire inventory of 54 Fast Growing SEHK Companies With High Insider Ownership here.

Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Contemplating Other Strategies?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:1302SEHK:2005SEHK:806 and

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]