Yuan Carry Trade Can Prosper Even After Yen Version Collapsed

(Bloomberg) -- The hugely popular yen carry trade crashed and burned this month as Japan’s currency surged. A less well-known version of the strategy is likely to be more immune to those kind of shocks.

Most Read from Bloomberg

Sydney Central Train Station Is Now an Architectural Destination

Nazi Bunker’s Leafy Makeover Turns Ugly Past Into Urban Eyecatcher

How the Corti?os of S?o Paulo Helped Shelter South America’s Largest City

Trades involving borrowing yuan to buy higher-yielding assets are set to be more resilient as China’s central bank keeps its monetary policy dovish, Royal Bank of Canada says. The yuan carry trade differs from the yen one as it mainly involves exporters and multinationals instead of speculators, Macquarie Group Ltd. data shows.

Carry trades, which involve seeking to capitalize on differences in global interest rates, became front and center of financial markets in early August as the unwind of the yen version fueled a selloff in risk assets. Investors cashed out after a Bank of Japan interest-rate hike bolstered the local currency, which in turn hammered the value of higher-yield targets such as the Mexican peso and Brazilian real.

“It still makes sense to short the yuan against a basket of emerging-market currencies as it would be contradictory to allow the currency to strengthen when the central bank is trying to ease policy,” said Alvin T. Tan, head of Asian currency strategy at Royal Bank of Canada in Singapore.

“China’s economy is struggling, and the PBOC is widely expected, and has indeed signaled, that it will ease policy further in coming months,” he said.

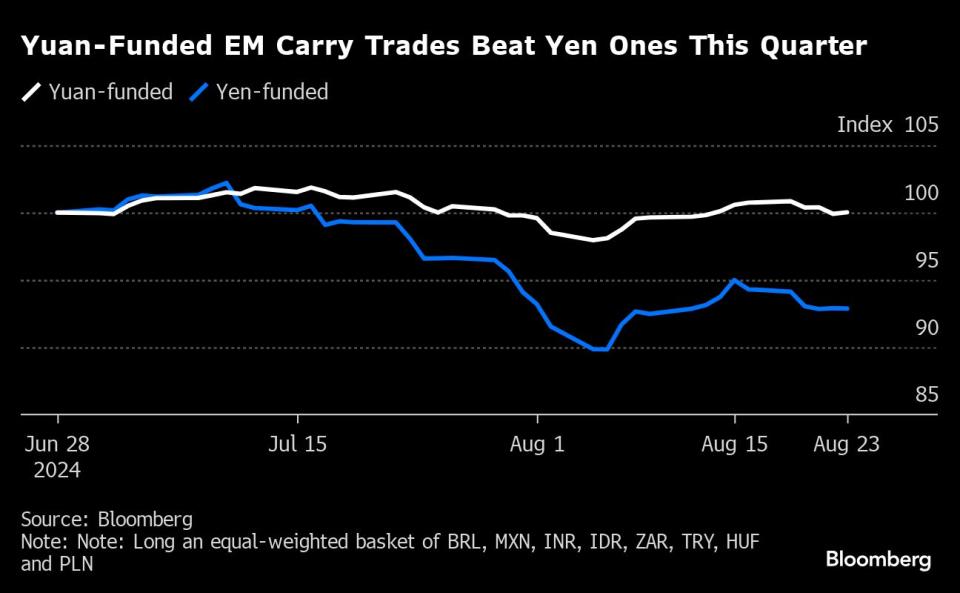

A carry trade that involves borrowing yuan and investing in a basket of eight emerging-market currencies has returned 0.5% this quarter even as the yen-funded alternative has tumbled around 7%, data compiled by Bloomberg show.

The collapse of the yen carry trade following the BOJ’s July 31 decision did at least initially spill over to the yuan. The yen surged 6.8% during the week through Aug. 5, while the yuan jumped 1.7%. Gains in the funding currency for a carry trade can wipe out possible returns.

Key Differences

There are a number of substantial underlying differences between the yuan and yen carry trades. The yuan isn’t fully convertible as the authorities limit the inflow and outflow of foreign currency to aid their control of the economy. That automatically crimps the size of the yuan carry trades compared to yen ones.

Secondly, while yen-funded trades are invested across a wide range of overseas targets, the vast proportion of those using borrowed yuan are held in dollars by Chinese exporters and multinational corporations. These only became profitable during 2022 after Federal Reserve rate hikes pushed US borrowing costs above Chinese ones.

Chinese exporters and multinationals have amassed over $500 billion in dollar holdings since 2022, according to Macquarie.

There are a number of reasons for investors to be attracted to the yuan carry trade, said Wee Khoon Chong, a senior Asia Pacific markets strategist at BNY in Hong Kong.

“The ongoing flush offshore yuan liquidity conditions might just make it too hard for market participants to resist reengaging in carry trades as and when market volatility subsides,” he said.

Still, the total size of yuan-funded carry trades may be limited as the People’s Bank of China has sufficient tools to prevent what it may see as an excessive buildup of speculative positions, Wee wrote in a client note this month.

“Will offshore yuan shorts be rebuilt? Sure, why not?” he said. “There will always be some opportunistic market participants out there but we do not see it to be significant size.”

Trade Recommendations

A number of financial firms are telling clients that borrowing yuan will continue to be a profitable method of funding carry positions.

Citigroup Inc. recently advised investors to bet on the Mexican peso and Brazilian real against the yuan and yen in the options market, according to a research report from strategists including Dirk Willer in New York.

Goldman Sachs Group Inc. and Nomura Holdings Inc. are also among those recommending investors short the yuan against a trade-weighted basket of other currencies due to China’s challenging macro headwinds and the softer US dollar backdrop.

What to Watch:

Hungary’s central bank will announce an interest-rate decision on Tuesday, while Israel’s policymakers will do the same on Wednesday

The Czech Republic and Poland will both release second-quarter GDP numbers, while Poland will also publish inflation data for August

China will publish August manufacturing PMI data, with the three previous prints all signaling contraction

Mexico’s central bank will release a quarterly inflation report.; Brazil is set to publish mid-month CPI data for August

Most Read from Bloomberg Businessweek

Losing Your Job Used to Be Shameful. Now It’s a Whole Identity

FOMO Frenzy Fuels Taiwan Home Prices Despite Threat of China Invasion

?2024 Bloomberg L.P.