The stage is set for the next 10% plunge in stocks

The stock market (^GSPC) continues to trend higher as earnings growth remains lackluster. This has caused valuations to get very expensive, signaling a stock market that’s becoming increasingly due for a sharp sell-off.

Everyone is flagging this anxiety-inducing pattern, and yet the market continues to rally arguably nonsensically.

“The S&P 500 has advanced 6.8% YTD (8.4% including dividends) despite a more modest improvement in the earnings outlook (+1.4%),” RBC’s Jonathan Golub observed in a note to clients on Monday. “Put differently, the market’s move higher has been fueled almost exclusively by multiples.”

Most analysts argue that these record-high stock prices are unsustainable without a significant pickup in earnings growth. Unfortunately, there isn’t much hope for that.

“Since EPS trends have typically been associated with S&P 500 index patterns, a sharper-than-expected uptick in profits would be a necessary prerequisite for additional upside,” Citi’s Tobias Levkovich said on Friday. “[A Citi survey suggests] new positive developments would need to emerge to justify more in terms of net income generation. With outstanding issues such as the impact of Brexit and/or fiscal policy post the US elections, it seems challenging to come to any powerful conclusions at this juncture.”

The Fed wants to hike, and the S&P fell 10% after the last hike.

Economic data in the US has been positive, highlighted by notably strong labor market and housing market data. This has put pressure on the Federal Reserve to tighten monetary policy with an interest rate hike sooner than later.

In fact, three members of the Fed have signaled that a hike will come sooner in just the past week. Last Tuesday, NY Fed President William Dudley said “we’re edging closer towards the point in time where it will be appropriate to raise rates further.” On Thursday, San Francisco Fed President John Williams said every meeting, including the one coming in September, should “be in play” for a rate hike. On Sunday, Fed Vice Chair Stanley Fischer said “we are close to our targets.”

“A more hawkish Fed could trigger a return of volatility if financial conditions (USD, credit spreads) start to deteriorate again,” Societe Generale’s Patrick Legland said on Monday. “The S&P 500 fell c.10% following the first rate hike last December.”

In that same breath, Legland warned of the importance of earnings to the stock market.

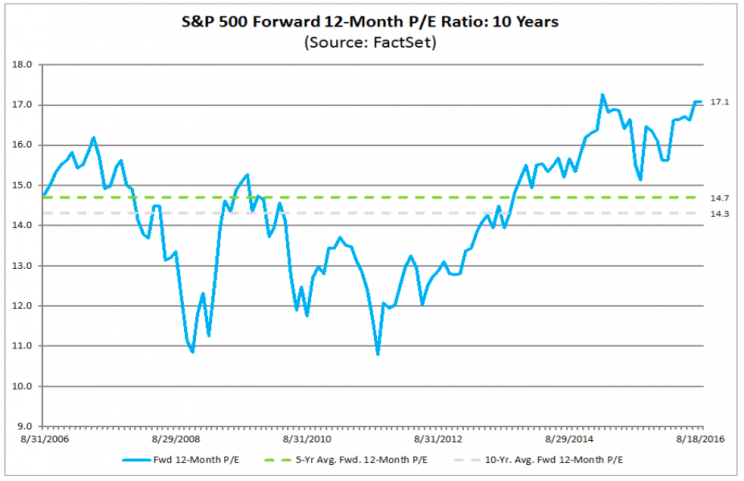

“US company earnings were better than expected in Q2,” he acknowledged. “But the sharp increase in valuation ratios (S&P 500 forward P/E 17x, P/B 2.9x) puts the onus on EPS growth at a time when global GDP growth remains uninspiring.”

Could fund flows save the day?

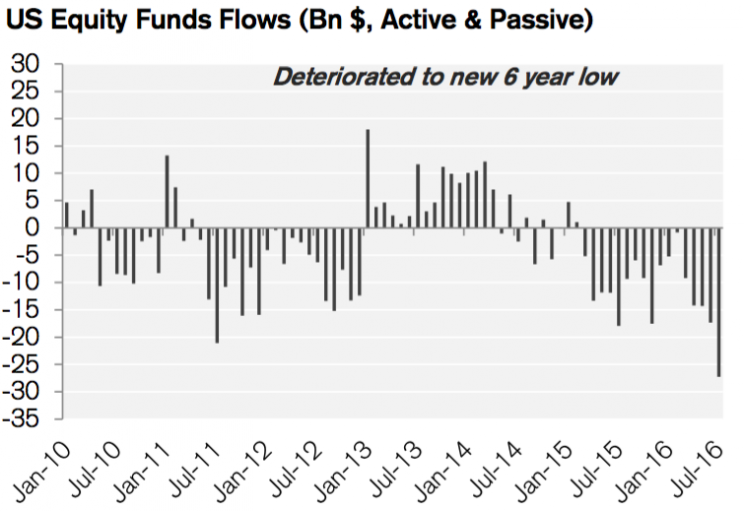

The sad thing about the current stock market rally is that it comes at a time when retail investors are spilling out of the stock market.

“US equity funds saw outflows deepen to a new 6 year low in July,” Credit Suisse’s Lori Calvasina observed on Thursday.

Perhaps this trend is set to turn around. Indeed, with bonds and bond funds offering little yield, no yield or even negative yield, perhaps we’ll finally witness the so-called “Great Rotation” of money out of bonds and into stocks.

“One way that share prices could surge would be to anticipate a new flow of money towards the fairly despised equity asset class,” Citi’s Levkovich posited.

But he isn’t betting on it.

“History suggests that substantive and sustained losses have to be taken by investors to ward off new money flows as aggressive growth fund outflows did not begin in earnest until roughly 17 months after the tech bubble peaked in March 2000,” he continued. “Home prices peaked in 2006 but people kept buying homes throughout 2007 and we suspect the same risk exists in bonds, especially those with negative yields, but losses will be taken before a major shift in sentiment occurs. People tend to be stubborn and are often creatures of habit, thus change takes time and this is the fate of the Great Rotation.”

So in summary: earnings are uninspiring, valuations are troubling, and fund flows are offering no hope.

Good luck trading this week, y’all.

–

Sam Ro is managing editor at Yahoo Finance.

Read more:

The peculiar pattern of S&P 500 earnings surprises

David Rosenberg nails the stock market in a perfect sentence

The stock market is making no sense for a lot of investors

How a bad story can cripple the economy

The gloomy profits narrative underlying the stock market just got worse

Forecasting 2017 earnings has become Wall Street’s most controversial task