Fortnox And 2 Other Swedish Stocks That Might Be Undervalued

The Swedish stock market has experienced mixed performance recently, with some sectors showing resilience despite broader economic uncertainties. Amidst this volatility, investors are increasingly on the lookout for stocks that may be undervalued and offer potential for growth. Identifying such stocks often involves assessing their financial health, growth prospects, and market position relative to current economic conditions. In this article, we will explore Fortnox and two other Swedish stocks that might be undervalued in today's market.

Top 10 Undervalued Stocks Based On Cash Flows In Sweden

Name | Current Price | Fair Value (Est) | Discount (Est) |

Sleep Cycle (OM:SLEEP) | SEK40.70 | SEK80.27 | 49.3% |

QleanAir (OM:QAIR) | SEK26.80 | SEK51.34 | 47.8% |

Scandi Standard (OM:SCST) | SEK82.10 | SEK161.97 | 49.3% |

Paradox Interactive (OM:PDX) | SEK139.20 | SEK261.67 | 46.8% |

Dometic Group (OM:DOM) | SEK68.40 | SEK132.98 | 48.6% |

Litium (OM:LITI) | SEK8.56 | SEK16.50 | 48.1% |

Flexion Mobile (OM:FLEXM) | SEK9.30 | SEK17.89 | 48% |

BE Group (OM:BEGR) | SEK53.50 | SEK106.15 | 49.6% |

Humble Group (OM:HUMBLE) | SEK9.445 | SEK18.66 | 49.4% |

Tourn International (OM:TOURN) | SEK8.54 | SEK16.48 | 48.2% |

Let's review some notable picks from our screened stocks.

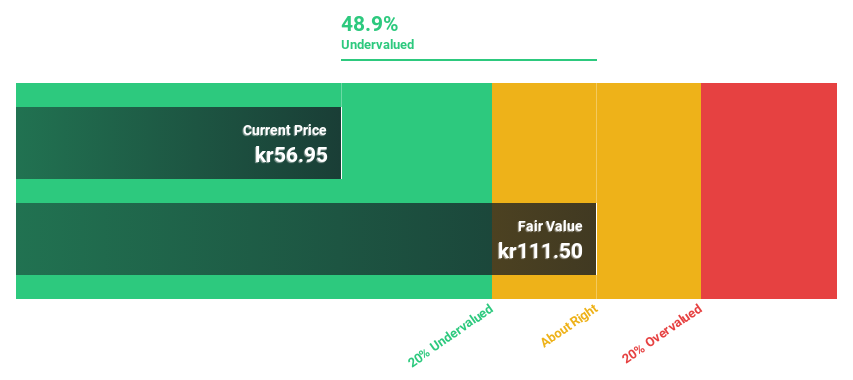

Fortnox

Overview: Fortnox AB (publ) offers financial and administrative software solutions for small and medium-sized businesses, accounting firms, and organizations, with a market cap of SEK38.94 billion.

Operations: Revenue segments include Businesses (SEK378 million), Marketplaces (SEK160 million), Core Products (SEK734 million), Accounting Firms (SEK352 million), and Financial Services (SEK249 million).

Estimated Discount To Fair Value: 25.4%

Fortnox (SEK63.84) is trading 25.4% below its estimated fair value of SEK85.62, indicating it may be undervalued based on cash flows. The company reported strong financials with Q2 sales at SEK515 million and net income at SEK164 million, both up significantly from last year. Earnings are forecast to grow 22.63% annually, outpacing the Swedish market's 15.7%, and revenue growth is projected at 19.8% per year, highlighting robust future prospects.

The growth report we've compiled suggests that Fortnox's future prospects could be on the up.

Delve into the full analysis health report here for a deeper understanding of Fortnox.

Nolato

Overview: Nolato AB (publ) develops, manufactures, and sells plastic, silicone, and thermoplastic elastomer products for various sectors including medical technology, pharmaceuticals, consumer electronics, telecom, automotive, hygiene, and other industries across Sweden and internationally with a market cap of SEK14.65 billion.

Operations: Medical Solutions generated SEK5.34 billion in revenue for the company.

Estimated Discount To Fair Value: 45.3%

Nolato (SEK54.4) is trading 45.3% below its estimated fair value of SEK99.36, making it highly undervalued based on cash flows. Recent earnings show steady performance with Q2 net income at SEK169 million compared to SEK155 million last year and basic EPS rising from SEK0.58 to SEK0.63. Earnings are forecasted to grow significantly at 23.35% per year, outpacing the Swedish market's 15.7%, despite a low future ROE of 14.6%.

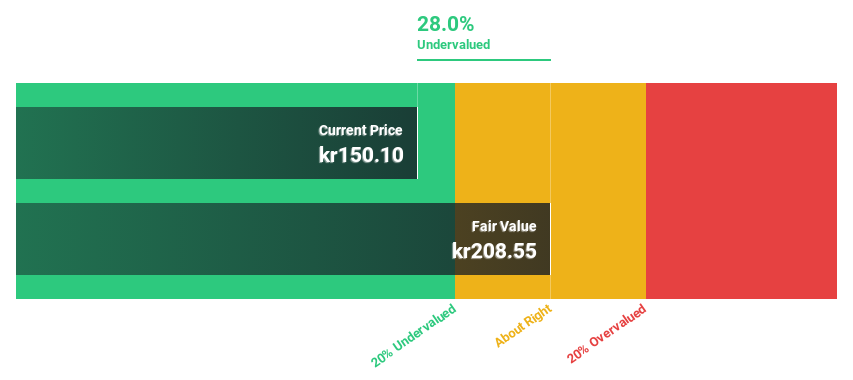

Sweco

Overview: Sweco AB (publ) is a global provider of architecture and engineering consultancy services with a market cap of approximately SEK58.92 billion.

Operations: Sweco generates revenue from various regions, including SEK8.74 billion from Sweden, SEK3.97 billion from Belgium, SEK3.67 billion from Finland, SEK3.50 billion from Norway, SEK3.24 billion from Denmark, SEK3.00 billion from the Netherlands, SEK2.71 billion from Germany & Central Europe, and SEK1.47 billion from the UK.

Estimated Discount To Fair Value: 28.7%

Sweco (SEK163.8) is trading 28.7% below its estimated fair value of SEK229.61, suggesting it is undervalued based on cash flows. Q2 earnings showed strong performance with net income rising to SEK540 million from SEK357 million a year ago and basic EPS increasing from SEK0.99 to SEK1.5. Earnings are forecasted to grow at 17.31% per year, outpacing the Swedish market's 15.7%, despite an unstable dividend track record and slower revenue growth at 5.5% per year.

The analysis detailed in our Sweco growth report hints at robust future financial performance.

Take a closer look at Sweco's balance sheet health here in our report.

Turning Ideas Into Actions

Embark on your investment journey to our 43 Undervalued Swedish Stocks Based On Cash Flows selection here.

Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Interested In Other Possibilities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include OM:FNOX OM:NOLA B and OM:SWEC B.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]