Is Home Depot Stock a Buy Now After Earnings?

The latest quarterly update from Home Depot (NYSE: HD) presented several mixed signals. While the home-improvement giant delivered a better-than-expected financial result, soft management guidance overshadowed the report. The stock is down about 8% from its 52-week high, highlighting ongoing consumer-spending uncertainties and the company's exposure to volatile housing-market conditions.

Are there enough positives in the outlook to outweigh near-term macroeconomic headwinds? Let's examine whether the recent sell-off offers a good opportunity to buy shares of Home Depot for your portfolio.

A cautious outlook from management

Home Depot has been defined by its resiliency in recent years, successfully supporting profitability through a shifting post-pandemic backdrop. This theme has been put to the test at the start of 2024.

In the second quarter, Home Depot posted earnings per share (EPS) of $4.67, coming in $0.12 ahead of the average Wall Street estimate and approximately flat from the prior-year quarter. Revenue of $43.2 billion increased by 1% year over year and was also above the consensus.

Those headline numbers are positive, but the context here is also important. In this case, Home Depot's acquisition of SRS Distributors in March added $1.3 billion in total Q2 revenue, while comparable sales in the U.S. decreased by a disappointing 3.6%. That includes a slowdown in customer traffic at stores as well as a lower average-sales ticket pricing.

The company has done a good job managing margins via cost-savings initiatives, but what it can't control is a more difficult operating environment. That was the message from Chief Executive Officer Ted Decker, describing weaker demand which warranted some caution. In the Q2 conference call, he said:

Higher interest rates and greater macro-economic uncertainty pressured consumer demand more broadly resulting in weaker spend across home improvement projects. When we look at the performance in the first six months of the year, as well as continued uncertainty around underlying consumer demand, we believe a more cautious sales outlook is warranted for the year.

Home Depot now expects full-year comparable sales to decrease between 3% and 4%, revised lower from the prior 1% decline forecast issued earlier this year. The company also sees 2024 adjusted EPS down by 1% to 3% from 2023, reversing the previous guidance for a 1% increase.

Home Depot at a premium valuation

Beyond the quarterly noise, it's fair to say that Home Depot fundamentals remain solid even if current trends are going through a rough patch. One strong point has been efforts to expand digital capabilities as online sales are up 4% over the past year.

There is also some enthusiasm with the SRS Distributors deal which management believes can be a growth driver for the company, marking an expansion and diversification into the professional building-supplies market.

Home Depot shares offer investors a 2.5% dividend yield, which is well supported by underlying free cash flow. Ultimately, the bullish case for the stock is that the company will emerge stronger as the economy improves, with potential Fed rate cuts into 2025 as a catalyst for a rebound in demand for consumer do-it-yourself home improvement activity.

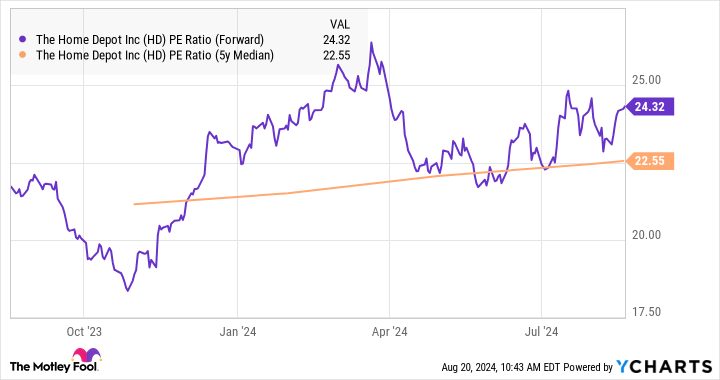

On the other hand, valuation is one area that deserves some attention. Home Depot stock is trading at approximately 24 times management's EPS guidance for 2024. Notably, this level is above the company's five-year average, which is closer to 23, implying that the stock is relatively expensive. That doesn't mean shares need to sell off from here, but it does make the upside more difficult in the near term.

It appears the market is giving the company the benefit of the doubt, already anticipating a recovery despite the lingering uncertainties. The main risk to consider is a scenario where conditions deteriorate further, forcing a reassessment lower in the earnings trajectory.

HD PE Ratio (Forward) data by YCharts.

Decision time for Home Depot Stock

I believe Home Depot stock deserves a hold rating for current shareholders, while investors thinking about adding a position may be better off with a wait-and-see approach. Until Home Depot shows evidence that comparable sales can turn positive as the key metric to watch, I expect shares to remain volatile.

Should you invest $1,000 in Home Depot right now?

Before you buy stock in Home Depot, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Home Depot wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $792,725!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 22, 2024

Dan Victor has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Home Depot. The Motley Fool has a disclosure policy.

Is Home Depot Stock a Buy Now After Earnings? was originally published by The Motley Fool