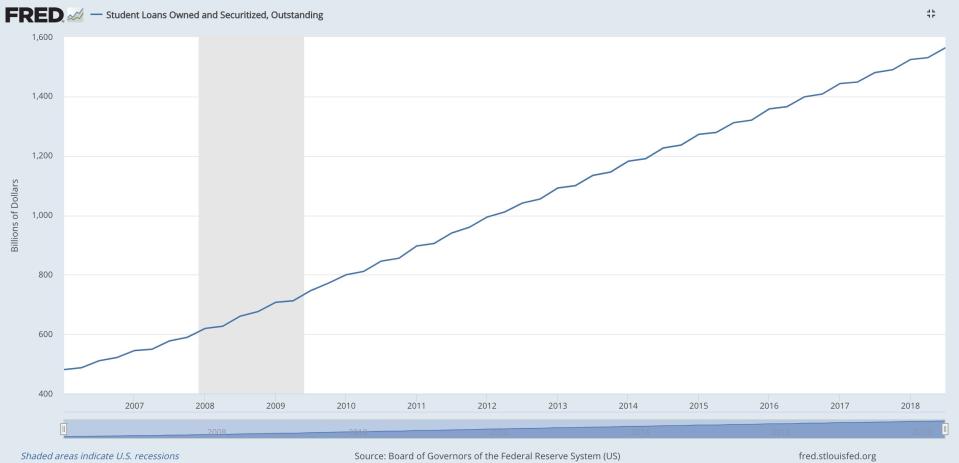

The $1.5 trillion student loan crisis isn’t going away. And one expert argues that the Trump administration is actually making it worse.

“The biggest challenge is just that this administration does not care about students,” Ben Miller, the senior director for post-secondary education at the Center for American Progress, told Yahoo Finance. “It wants to side with companies and ignore the plight of individuals. It’s hard for me to imagine a world where they suddenly develop sympathy for people after having shown none of it for almost two years.”

Miller explained that, until last year, the Consumer Finance Protection Bureau (CFPB) had been serving a helpful role in monitoring the student loan system by recommending regulations at both the state and federal level. When Seth Frotman resigned as the the CFPB’s Student Loan Ombudsman in August, that potential for regulation went by the wayside.

The CFPB “did a bunch of reports about public-service loan forgiveness and were flagging things like ... the ways the payments are being tracked that are wrong and create a major problem,” Miller said. Now, “they don’t seem to have any interest in doing that, per the resignation letter from Seth Frotman.”

And even before Frotman’s resignation, the Department of Education cut off a lot of their information-sharing with the CFPB. That made matters worse, given that consumer protections like those the CFPB had been tracking are one way to ensure damaging lending tactics and advice stay out of the student loan system.

“There’s not enough being done to make sure that, when a borrower calls to say ‘I’m struggling,’ their servicer properly guides them and has the proper incentives to fix that borrower’s problem in a way that sets them up for long-term success,” said Miller, who wrote a New York Times op-ed titled “The Student Debt Problem Is Worse Than We Imagined“ in 2018.

“In some cases, I think the problem is that the Department of Education has not properly guided servicers on how to administer certain things,” such as public-service loan forgiveness, Miller explained. “The servicers running [that] program needed to be given more explicit guidance on how to actually run it.”

‘Loan servicing is … sort of like Walmart’

When it comes to long-term success, the key lies in holding loan servicers accountable to the borrowers and increasing the amount of government oversight of the loan servicing system. Since 2010, all student loans “have been made directly by the US Department of Education, which means that the Department hires and oversees the contractors who handle the loans,” including Navient.

In that, “loan servicing is a funny business in that it’s sort of like Walmart,” Miller said. “It’s all about volume.”

He explained that Navient and companies like it are rewarded by the Department of Education in terms of the number of loans they provide, based on the individual’s status as a borrower. Navient, for example, handles the loans of 12 million borrowers.

“The most a servicer can get per borrower [from the federal government] is $2.85,” Miller said. “The way you have a sustainable business in servicing is to have as many borrowers as possible.”

‘Versus 3 minutes to get them into forbearance‘

When any one servicer is handling large numbers of borrowers, the incentive is to work through customer service calls as quickly as possible. In some cases, this leaves a borrower without information that is more applicable to his or her personal loan situation.

As previously reported by the Associated Press, a Department of Education audit found that loan servicer Navient often recommended forbearance, in which borrowers are “responsible for paying the interest that accrues on all types of federal student loans.” Alternative repayment plans could prevent borrowers from paying more. Deferment, for example, allows the student to forego the interest on certain types of loans.

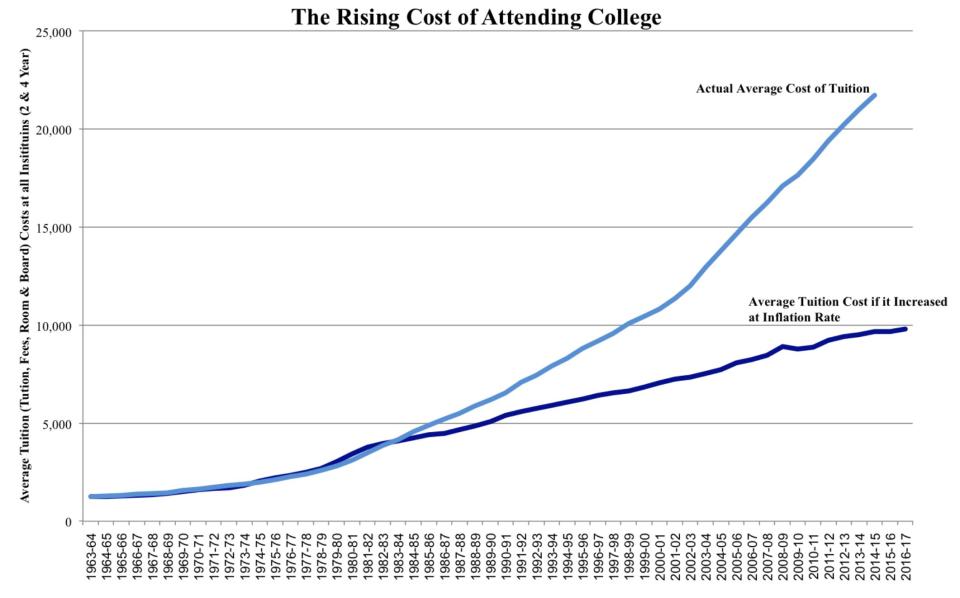

All of this occurred as the cost of higher education ballooned.

“If it takes someone 15 minutes to end up putting a borrower in income-based repayment versus 3 minutes to get them into forbearance,” the servicer is going to recommend forbearance in order to reach as many callers as possible, whether or not that individual will benefit the most from that recommendation.

Basically, offering forbearance is an immediate fix for what becomes a lifelong problem for many student borrowers.

According to Miller, the government’s process of holding servicers accountable does not include asking: “Are those borrowers current? Do they get the right advice, or are they just kept current through artificial means? If someone sends in documents to get them reviewed and put on income-based repayment, are they done quickly?”

Runaway interest inflates student debt

Colleen May, a 24-year-old borrower who graduated with a bachelor’s degree from a Pennsylvania university in 2016, said she was “not made aware that my loans would accumulate interest while in deferment,” and ended up owing more that her initial balance.

“A lot of my loans were actually paid off with a store credit card,” May told Yahoo Finance. That’s because the card had an introductory 0% interest rate. “But they were a pain,” she explained, since the credit card payments had to be made before the special interest rate offer ended.

In the two-and-a-half years since she graduated, May has paid down her $41,000 debt to $10,000. “But that’s with paying $1,600 a month, compared to my minimum payment of $150.”

Had she only been paying the minimum, May wouldn’t completely pay off her student debt until 2026, a full 10 years after completing her degree.

The loan burdens are weighing on a generation of potential homeowners. A report from the Federal Reserve cites student debt as the reason 400,000 young people didn’t own homes by 2014. The Fed found that a “$1,000 increase in student loan debt... causes a 1 to 2 percentage point drop in the homeownership rate for student loan borrowers during their late 20s and early 30s.”

‘We’ve forced people to borrow’

One of the biggest issues within the higher education loan system comes down to one fact: many borrowers shouldn’t be borrowers to begin with.

“A major problem that we have with our loan system is that we’ve forced people to borrow that we should have given grant aid to,” Miller said.

Figuring out what kind of aid for which a student is qualified creates a lot of confusion, and takes a lot of research to understand — especially considering most Americans begin their undergraduate careers at 18 years old, without ever having dealt with this kind of financial burden before.

“The challenge,” Miller said, “is that we’ve been getting a pretty clear message from the administration that there’s not a ton of interest in really standing up for borrowers now.”

READ MORE:

'It gets confusing fast': FAFSA financial aid for students, explained

Former U.S. official: The student debt system is 'a nightmare'

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, YouTube, and reddit.